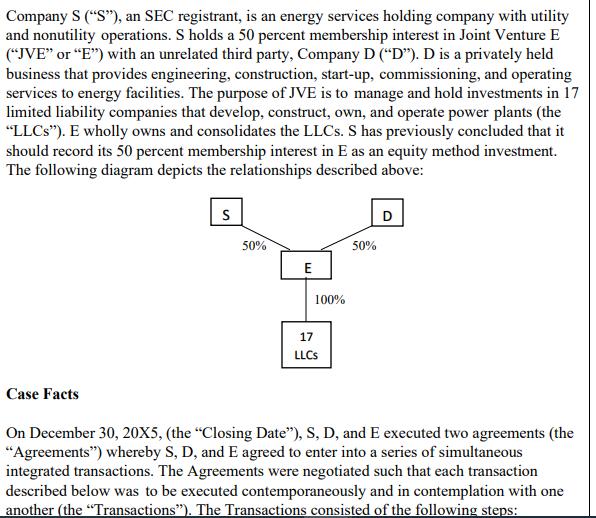

Company S (S), an SEC registrant, is an energy services holding company with utility and nonutility operations. S holds a 50 percent membership interest

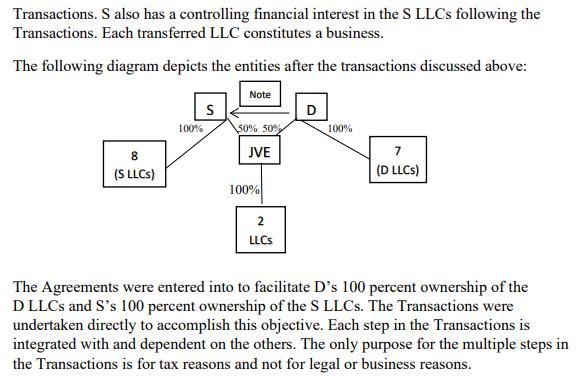

Company S ("S"), an SEC registrant, is an energy services holding company with utility and nonutility operations. S holds a 50 percent membership interest in Joint Venture E ("JVE" or "E") with an unrelated third party, Company D ("D"). D is a privately held business that provides engineering, construction, start-up, commissioning, and operating services to energy facilities. The purpose of JVE is to manage and hold investments in 17 limited liability companies that develop, construct, own, and operate power plants (the "LLCS"). E wholly owns and consolidates the LLCs. S has previously concluded that it should record its 50 percent membership interest in E as an equity method investment. The following diagram depicts the relationships described above: Case Facts S 50% E 100% 17 LLCS 50% D On December 30, 20X5, (the "Closing Date"), S, D, and E executed two agreements (the "Agreements") whereby S, D, and E agreed to enter into a series of simultaneous integrated transactions. The Agreements were negotiated such that each transaction described below was to be executed contemporaneously and in contemplation with one another (the "Transactions"). The Transactions consisted of the following steps: E distributed on a pro rata basis to both S and D a 50 percent membership interest in 15 of the LLCs (subsequently referred to as the "Transferred LLCS"). The remaining two LLCs will remain 100 percent owned by E after the Transactions. S sold to D its 50 percent membership interest in seven of the Transferred LLCs in exchange for a note and a 50 percent membership interest in the remaining eight Transferred LLCs. The end result of the Transactions is that D will directly own 100 percent of seven of the Transferred LLCs (the "D LLCs"), and S will directly own 100 percent of eight of the Transferred LLCs (the "S LLCs") and will hold a note receivable from D (the "Note"). S will retain its equity method investment in E and an indirect 50 percent interest in the remaining two LLCs that remain 100 percent owned by E after the Transactions. S also has a controlling financial interest in the S LLCs following the Transactions. Each transferred LLC constitutes a business. The following diagram depicts the entities after the transactions discussed above: Note 8 (S LLCs) 100% S 50% 50% JVE 100% 2 LLCS D 100% 7 (D LLCs) The Agreements were entered into to facilitate D's 100 percent ownership of the DLLCs and S's 100 percent ownership of the S LLCs. The Transactions were undertaken directly to accomplish this objective. Each step in the Transactions is integrated with and dependent on the others. The only purpose for the multiple steps in the Transactions is for tax reasons and not for legal or business reasons. Required: 1. In the determination of the appropriate accounting, should the Transactions be considered a single transaction or multiple transactions? 2. How should E account for the Transactions? 3. How should S account for its previously held indirect interest in the S LLCs and the net assets of the S LLCs acquired?

Step by Step Solution

3.50 Rating (167 Votes )

There are 3 Steps involved in it

Step: 1

It is recommended that the Transactions be treated as a single transaction for the purpose of determ...

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Authors: Arlen Langvardt, A. James Barnes, Jamie Darin Prenkert, Martin A. McCrory

17th edition

1259917118, 978-1259917110