Compare and contrast the differences between Limited Liability Corporations, Limited Liability Partnership, and Sole Proprietorships.

Be sure to discuss benefits, disadvantages and thoroughly explain what they are individualy. Use google, articles and chart listed below.

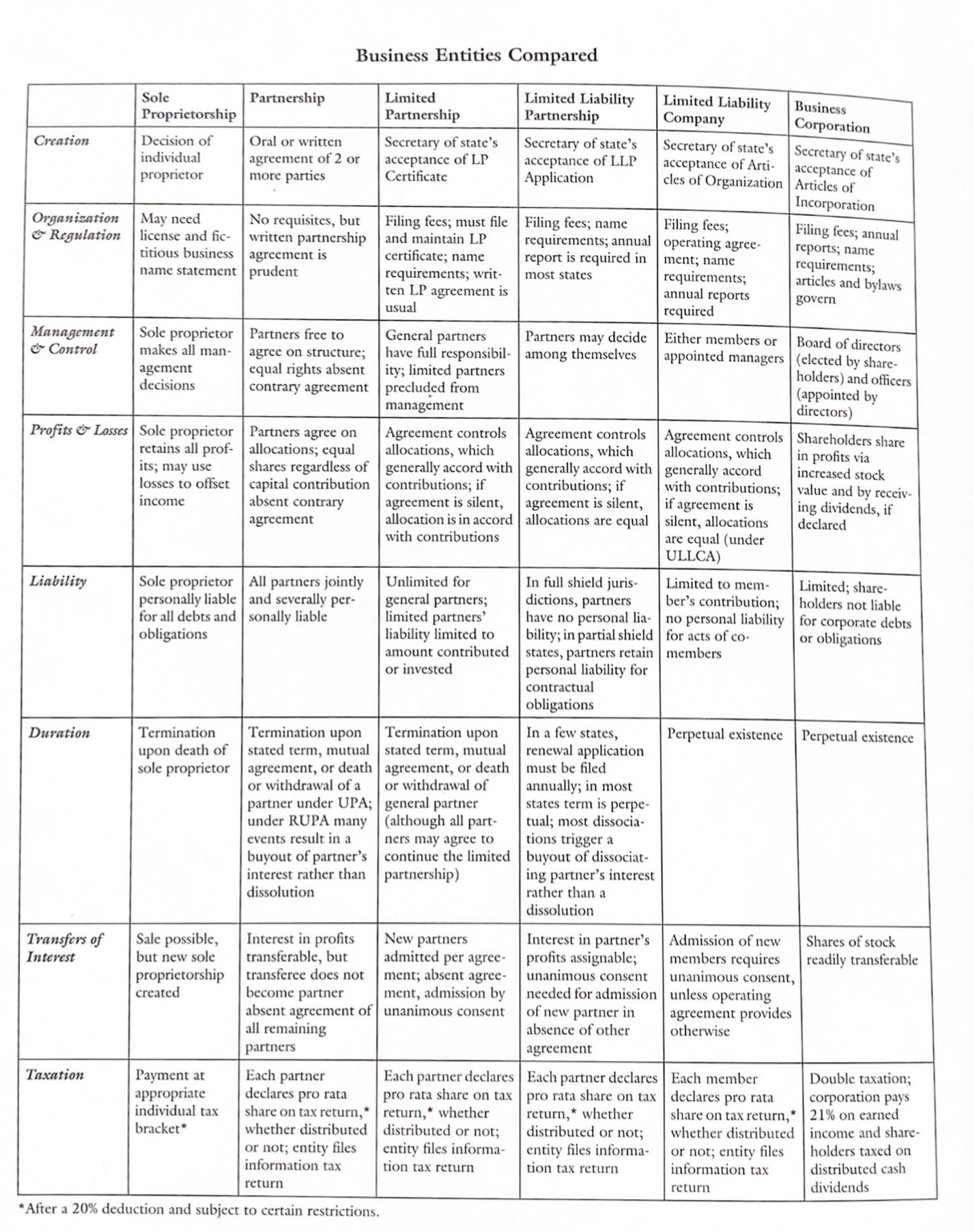

Business Entities Compared Sole Partnership Limited Limited Liability Limited Liability Business Proprietorship Partnership Partnership Company Corporation Creation Decision of Oral or written Secretary of state's Secretary of state's Secretary of state's Secretary of state's individual agreement of 2 or acceptance of LP acceptance of LLP acceptance of Arti- acceptance of proprietor more parties Certificate Application cles of Organization Articles of Incorporation Organization May need No requisites, but Filing fees; must file Filing fees; name Filing fees; Filing fees; annual & Regulation license and fic- written partnership and maintain LP requirements; annual | operating agree- reports; name titious business agreement is certificate; name report is required in ment; name requirements; name statement |prudent requirements; writ- most states requirements; articles and bylaws ten LP agreement is annual reports govern usual required Management Sole proprietor Partners free to General partners Partners may decide Either members or Board of directors Control makes all man- agree on structure; have full responsibil among themselves appointed managers (elected by share- agement equal rights absent ity; limited partners holders) and officers decisions contrary agreement precluded from (appointed by management directors Profits & Losses Sole proprietor Partners agree on Agreement controls Agreement controls Agreement controls Shareholders share retains all prof- allocations; equal allocations, which allocations, which allocations, which in profits via its; may use shares regardless of generally accord with | generally accord with | generally accord increased stock losses to offset capital contribution contributions; if contributions; if with contributions; value and by receiv- income absent contrary agreement is silent, agreement is silent, if agreement is ing dividends, if agreement allocation is in accord | allocations are equal silent, allocations declared with contributions are equal (under ULLCA Liability Sole proprietor All partners jointly Unlimited for In full shield juris- Limited to mem- Limited; share personally liable | and severally per- general partners; dictions, partners ber's contribution; holders not liable for all debts and sonally liable limited partners' have no personal lia- no personal liability for corporate debts obligations liability limited to bility; in partial shield | for acts of co- or obligations amount contributed states, partners retain| members or invested personal liability for contractual obligations Duration Termination Termination upon Termination upon In a few states, Perpetual existence Perpetual existence upon death of stated term, mutual stated term, mutual renewal application sole proprietor agreement, or death | agreement, or death must be filed or withdrawal of a or withdrawal of annually; in most partner under UPA; general partner states term is perpe- under RUPA many (although all part- ual; most dissocia- events result in a ners may agree to tions trigger a buyout of partner's continue the limited buyout of dissociat- interest rather than partnership) ing partner's interest dissolution rather than a dissolution Transfers of Sale possible, Interest in profits New partners Interest in partner's Admission of new Shares of stock Interest but new sole transferable, but admitted per agree- profits assignable; members requires readily transferable proprietorship transferce does not ment; absent agree- unanimous consent unanimous consent, created become partner ment, admission by needed for admission | unless operating absent agreement of |unanimous consent of new partner in agreement provides all remaining absence of other otherwise partners agreement Taxation Payment at Each partner Each partner declares Each partner declares Each member Double taxation; appropriate declares pro rata pro rata share on tax | pro rata share on tax | declares pro rata corporation pays individual tax share on tax return,* return, * whether return, * whether share on tax return,* 21% on earned bracket* whether distributed distributed or not; distributed or not; whether distributed income and share- or not; entity files entity files informa- entity files informa- or not; entity files holders taxed on information tax tion tax return tion tax return information tax distributed cash return return dividends *After a 20% deduction and subject to certain restrictions