Answered step by step

Verified Expert Solution

Question

1 Approved Answer

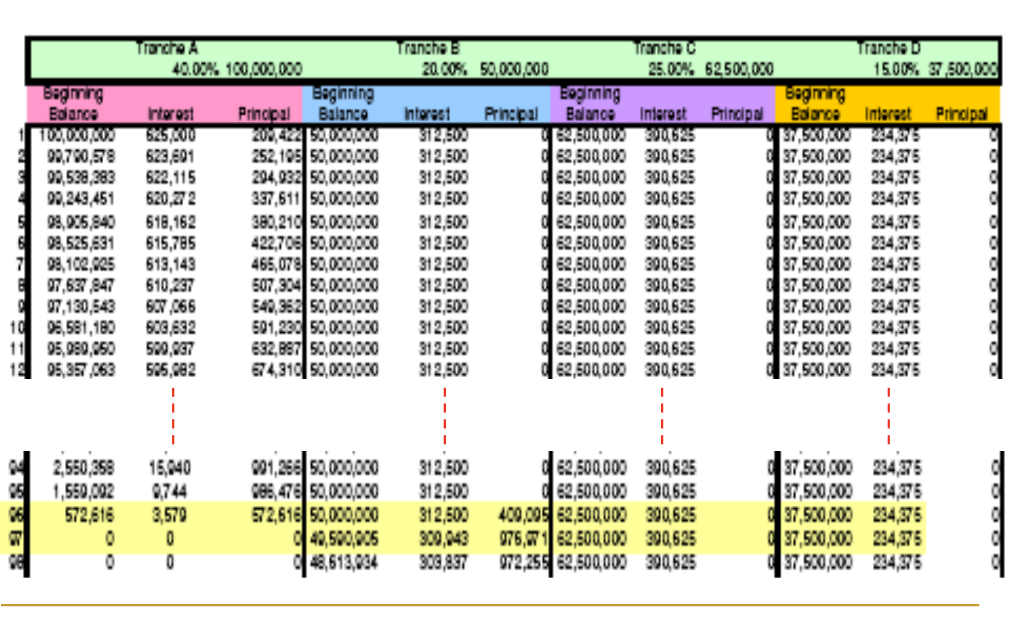

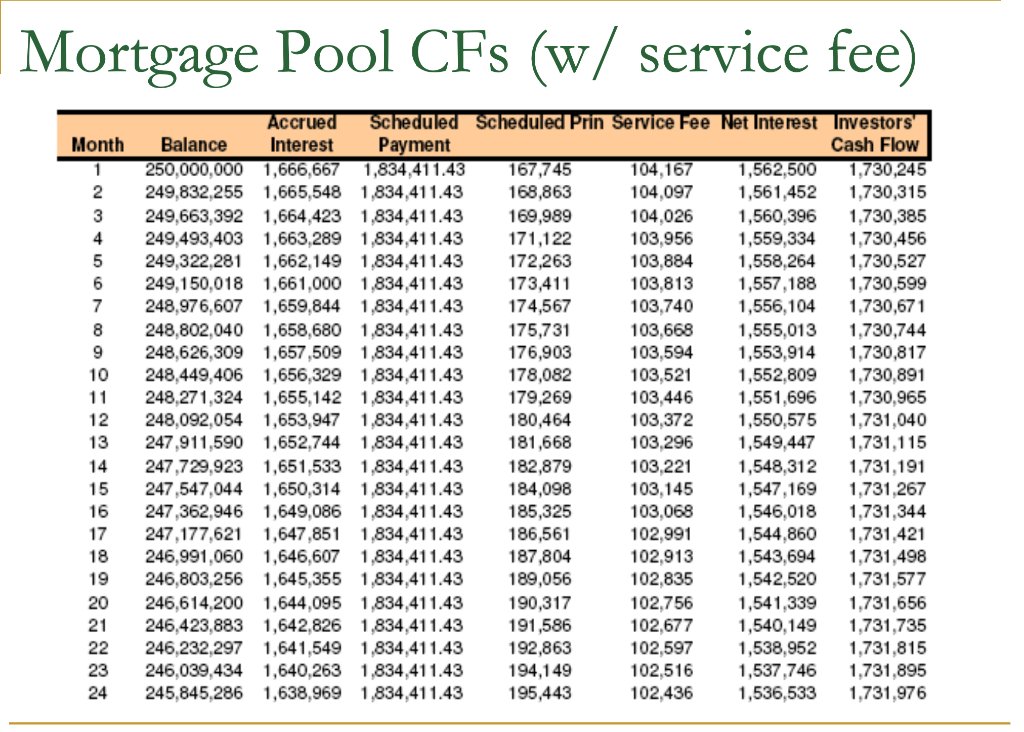

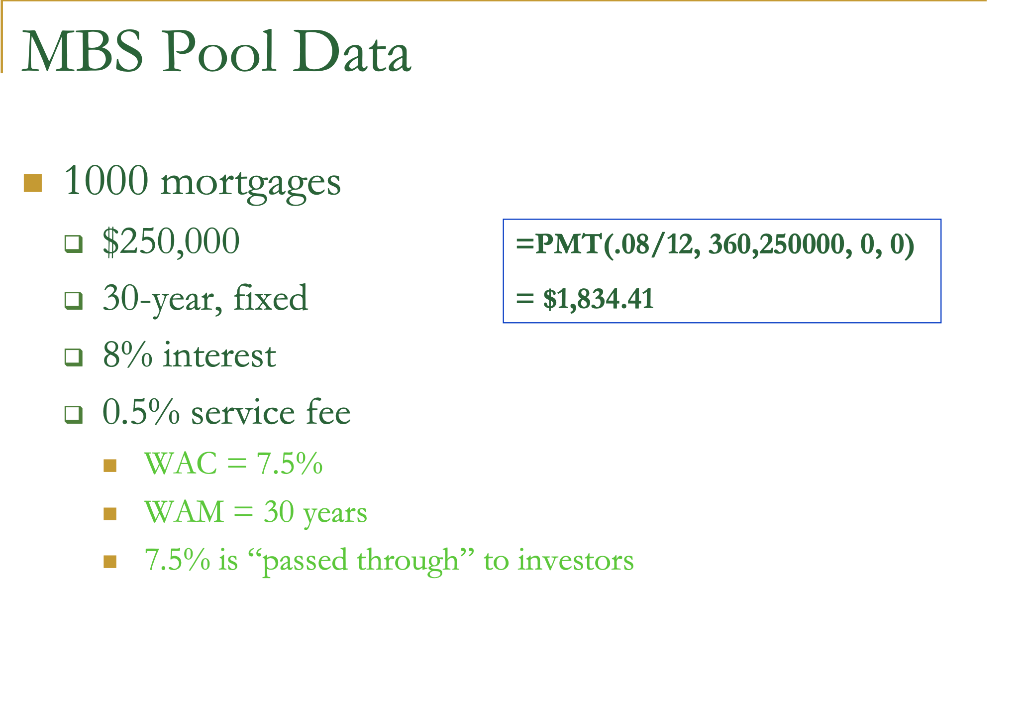

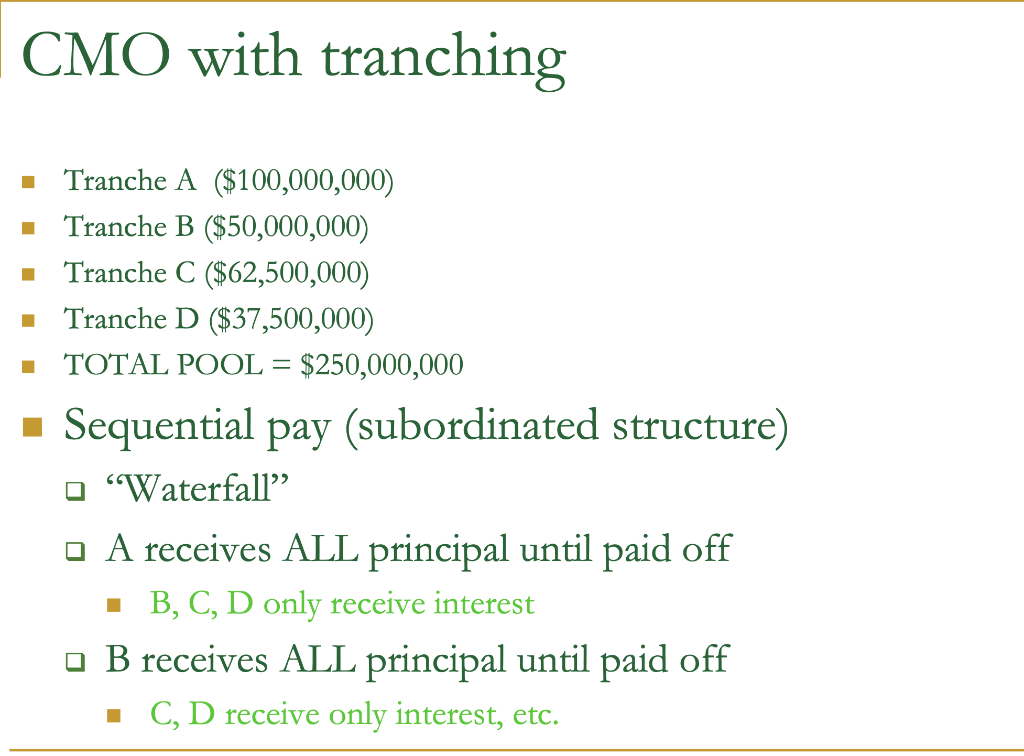

Complete dynamic model for 4 tranches (waterfall structure) as described in class Mortgage Pool CFs (w/ service fee) MBS Pool Data 1000 mortgages $250,00030-year,fixed=PMT(.08/12,360,250000,0,0)=$1,834.41 8%

Complete dynamic model for 4 tranches (waterfall structure) as described in class

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Dynamic Asset Allocation With Forwards And Futures

Authors: Abraham Lioui , Patrice Poncet

1st Edition

0387241078,038724106X