Question

Complete the binomial tree to price ATM European and American put options on a non-dividend-paying index with 3-month maturity in three steps. The index is

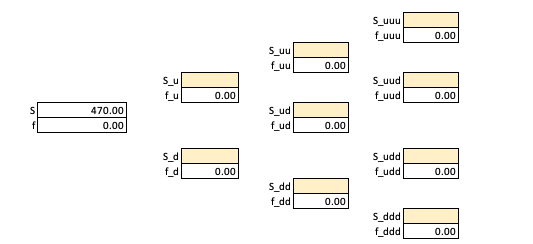

Complete the binomial tree to price ATM European and American put options on a non-dividend-paying index with 3-month maturity in three steps. The index is currently priced at $470 with 17.5% volatility and the risk-free rate is 0.25%.

S0= 470. K = 470. r= 0.25% T=0.25 Sigma= 0.175

What is Delta T, u, and d for the binomial tree

Suuu fuuu 0.00 Suu f_uu 0.00 Suud S_u fu 0.00 f uud 0.00 470.00 0.00 S_ud f_ud 0.00 s_d fd S_udd f_udd 0.00 0.00 S_dd f dd 0.00 S_ddd f_ddd 0.00 Suuu fuuu 0.00 Suu f_uu 0.00 Suud S_u fu 0.00 f uud 0.00 470.00 0.00 S_ud f_ud 0.00 s_d fd S_udd f_udd 0.00 0.00 S_dd f dd 0.00 S_ddd f_ddd 0.00Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Big Tech In Finance

Authors: Igor Pejic

1st Edition

139860898X, 978-1398608986