Compose a memo from Orville Wright to Amelia Earhart on December 31, 2021. State your investment recommendation and your rationale for making it.

(Please use the spreadsheet that I calculated)

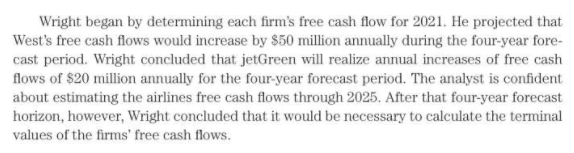

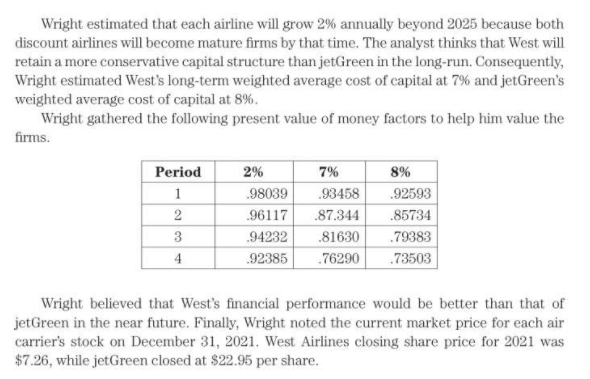

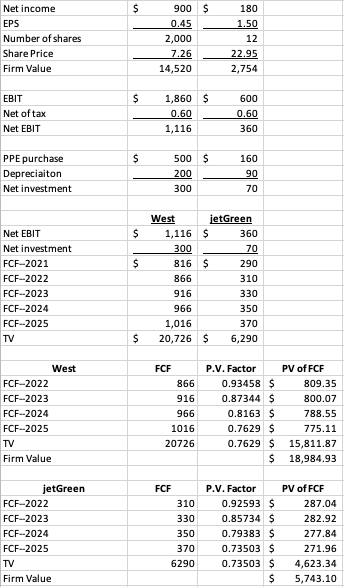

Orville Wright analyzes the airline industry. Investors with an interest in or lending to airlines seek his advice and recommendations. Amelia Earhart, Orville's wealthiest client, asked him to determine which of two airlines offered her the better investment opportu- nity at the end of 2021. Amelia's interest centered on two of the so-called discount airlines. West Airlines was created after the United States deregulated the airline industry. Prior to deregula- tion, airlines priced tickets on a cost-plus basis. This arrangement allowed carriers to recover all of their costs and earn acceptable profit margins and returns on investment. In this environment older legacy carriers, such as American, Delta, and United, did not have an incentive for containing costs. The air carriers merely passed on those cost to their passengers in the form of ever escalating ticket prices. Mounting pressure from the public spurred Congress to substantially deregulate the passenger airline industry in the late 1970s. Sensing an opportunity to capitalize on airline deregulation, investors formed West Airlines. This post-regulatory start-up's business model focused on containing costs, such as non-unionized labor, and passing the cost savings on to their passengers in the form of lower ticket prices. The strategy proved financially successful as West gained market share from the legacy carriers and stimulated demand in consumers who previously did not utilize air travel. The financial success of West spawned other discount competitors, the most successful of which was jetGreen Airlines. Amelia Earhart wanted to purchase stock in either West or jetGreen. She paid Orville Wright for his analysis and recommendation. Orville begins his assignment by gathering the most recent financial statements for West and jetGreen Airlines (amounts in millions, except earnings per share): Wright began by determining each firm's free cash flow for 2021. He projected that West's free cash flows would increase by $50 million annually during the four-year fore- cast period. Wright concluded that jetGreen will realize annual increases of free cash flows of $20 million annually for the four-year forecast period. The analyst is confident about estimating the airlines free cash flows through 2025. After that four-year forecast horizon, however, Wright concluded that it would be necessary to calculate the terminal values of the firms' free cash flows. Wright estimated that each airline will grow 2% annually beyond 2025 because both discount airlines will become mature firms by that time. The analyst thinks that West will retain a more conservative capital structure than jetGreen in the long-run. Consequently, Wright estimated West's long-term weighted average cost of capital at 7% and jetGreen's weighted average cost of capital at 8%. Wright gathered the following present value of money factors to help him value the firms. Period 1 2 3 4 2% -98039 .96117 .94232 .92385 7% 93458 .87.344 .81630 .76290 8% .92593 .85734 .79383 .73503 Wright believed that West's financial performance would be better than that of jetGreen in the near future. Finally, Wright noted the current market price for each air carrier's stock on December 31, 2021. West Airlines closing share price for 2021 was $7.26, while jetGreen closed at $22.95 per share. $ Net income EPS Number of shares Share Price Firm Value 900 $ 0.45 2,000 7.26 14,520 180 1.50 12 22.95 2,754 $ EBIT Net of tax Net EBIT 1,860 $ 0.60 1,116 600 0.60 360 $ PPE purchase Depreciaiton Net investment 500 $ 200 300 160 90 70 $ $ Net EBIT Net investment FCF-2021 FCF-2022 FCF-2023 FCF-2024 FCF-2025 TV West jetGreen 1,116 $ 360 300 70 816 $ 290 866 310 916 330 966 350 1,016 370 20,726 $ 6,290 $ West FCF-2022 FCF-2023 FCF-2024 FCF-2025 TV Firm Value FCF 866 916 966 P.V. Factor 0.93458 $ 0.87344 $ 0.8163 $ 0.7629 $ 0.7629 $ $ PV of FCF 809.35 800.07 788.55 775.11 15,811.87 18,984.93 1016 20726 jetGreen FCF--2022 FCF-2023 FCF-2024 FCF-2025 TV Firm Value FCF 310 330 350 370 6290 P.V. Factor 0.92593 $ 0.85734 $ 0.79383 $ 0.73503 $ 0.73503 $ $ PV of FCF 287.04 282.92 277.84 271.96 4,623.34 5,743.10 Firm Value Bonds payable Common equity value Number of shares Intrinsic share value EPS Intrinsic P/E Ratio West jetGreen $ 18,985.24 $ 5,743.10 4,000.00 3,000.00 $ 14,985.24 $ 2,743.00 2000 120 $ 7.49 $ 22.86 $ 0.45 $ 1.50 16.65 15.24 Orville Wright analyzes the airline industry. Investors with an interest in or lending to airlines seek his advice and recommendations. Amelia Earhart, Orville's wealthiest client, asked him to determine which of two airlines offered her the better investment opportu- nity at the end of 2021. Amelia's interest centered on two of the so-called discount airlines. West Airlines was created after the United States deregulated the airline industry. Prior to deregula- tion, airlines priced tickets on a cost-plus basis. This arrangement allowed carriers to recover all of their costs and earn acceptable profit margins and returns on investment. In this environment older legacy carriers, such as American, Delta, and United, did not have an incentive for containing costs. The air carriers merely passed on those cost to their passengers in the form of ever escalating ticket prices. Mounting pressure from the public spurred Congress to substantially deregulate the passenger airline industry in the late 1970s. Sensing an opportunity to capitalize on airline deregulation, investors formed West Airlines. This post-regulatory start-up's business model focused on containing costs, such as non-unionized labor, and passing the cost savings on to their passengers in the form of lower ticket prices. The strategy proved financially successful as West gained market share from the legacy carriers and stimulated demand in consumers who previously did not utilize air travel. The financial success of West spawned other discount competitors, the most successful of which was jetGreen Airlines. Amelia Earhart wanted to purchase stock in either West or jetGreen. She paid Orville Wright for his analysis and recommendation. Orville begins his assignment by gathering the most recent financial statements for West and jetGreen Airlines (amounts in millions, except earnings per share): Wright began by determining each firm's free cash flow for 2021. He projected that West's free cash flows would increase by $50 million annually during the four-year fore- cast period. Wright concluded that jetGreen will realize annual increases of free cash flows of $20 million annually for the four-year forecast period. The analyst is confident about estimating the airlines free cash flows through 2025. After that four-year forecast horizon, however, Wright concluded that it would be necessary to calculate the terminal values of the firms' free cash flows. Wright estimated that each airline will grow 2% annually beyond 2025 because both discount airlines will become mature firms by that time. The analyst thinks that West will retain a more conservative capital structure than jetGreen in the long-run. Consequently, Wright estimated West's long-term weighted average cost of capital at 7% and jetGreen's weighted average cost of capital at 8%. Wright gathered the following present value of money factors to help him value the firms. Period 1 2 3 4 2% -98039 .96117 .94232 .92385 7% 93458 .87.344 .81630 .76290 8% .92593 .85734 .79383 .73503 Wright believed that West's financial performance would be better than that of jetGreen in the near future. Finally, Wright noted the current market price for each air carrier's stock on December 31, 2021. West Airlines closing share price for 2021 was $7.26, while jetGreen closed at $22.95 per share. $ Net income EPS Number of shares Share Price Firm Value 900 $ 0.45 2,000 7.26 14,520 180 1.50 12 22.95 2,754 $ EBIT Net of tax Net EBIT 1,860 $ 0.60 1,116 600 0.60 360 $ PPE purchase Depreciaiton Net investment 500 $ 200 300 160 90 70 $ $ Net EBIT Net investment FCF-2021 FCF-2022 FCF-2023 FCF-2024 FCF-2025 TV West jetGreen 1,116 $ 360 300 70 816 $ 290 866 310 916 330 966 350 1,016 370 20,726 $ 6,290 $ West FCF-2022 FCF-2023 FCF-2024 FCF-2025 TV Firm Value FCF 866 916 966 P.V. Factor 0.93458 $ 0.87344 $ 0.8163 $ 0.7629 $ 0.7629 $ $ PV of FCF 809.35 800.07 788.55 775.11 15,811.87 18,984.93 1016 20726 jetGreen FCF--2022 FCF-2023 FCF-2024 FCF-2025 TV Firm Value FCF 310 330 350 370 6290 P.V. Factor 0.92593 $ 0.85734 $ 0.79383 $ 0.73503 $ 0.73503 $ $ PV of FCF 287.04 282.92 277.84 271.96 4,623.34 5,743.10 Firm Value Bonds payable Common equity value Number of shares Intrinsic share value EPS Intrinsic P/E Ratio West jetGreen $ 18,985.24 $ 5,743.10 4,000.00 3,000.00 $ 14,985.24 $ 2,743.00 2000 120 $ 7.49 $ 22.86 $ 0.45 $ 1.50 16.65 15.24