Question

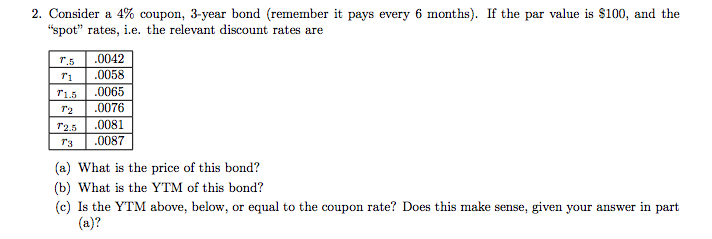

Consider a 4% coupon, 3-year bond (remember it pays every 6 months). If the par value is $100, and the spot rates, i.e. the relevant

Consider a 4% coupon, 3-year bond (remember it pays every 6 months). If the par value is $100, and the "spot" rates, i.e. the relevant discount rates are

r.5 = .0042

r1 = .0058

r1.5 = .0065

r2 = .0076

r2.5 = .0081

r3 = .0087

a. What is the price of this bond?

b. What is the YTM of this bond?

c. Is the YTM above, below, or equal to the coupon rate? Does this make sense, given your answer in part (a)?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Monetary Policy Strategy

Authors: Frederic S. Mishkin

1st Edition

0262513374, 978-0262513371