Answered step by step

Verified Expert Solution

Question

1 Approved Answer

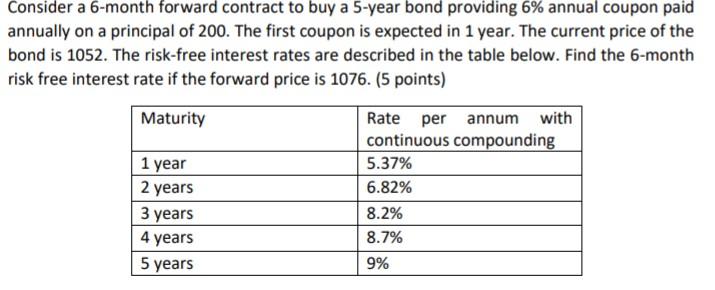

Consider a 6-month forward contract to buy a 5-year bond providing 6% annual coupon paid annually on a principal of 200. The first coupon

Consider a 6-month forward contract to buy a 5-year bond providing 6% annual coupon paid annually on a principal of 200. The first coupon is expected in 1 year. The current price of the bond is 1052. The risk-free interest rates are described in the table below. Find the 6-month risk free interest rate if the forward price is 1076. (5 points) Maturity 1 year 2 years 3 years 4 years 5 years Rate per annum with continuous compounding 5.37% 6.82% 8.2% 8.7% 9%

Step by Step Solution

★★★★★

3.47 Rating (163 Votes )

There are 3 Steps involved in it

Step: 1

Solution To solve this problem we can use the formula for the forward price of a bond Forward price ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Advanced Accounting

Authors: Paul M. Fischer, William J. Tayler, Rita H. Cheng

11th edition

538480289, 978-0538480284