Question: Consider a 6-year 5.5% coupon bond that is rated BBB when issued at par (i.e., $1,000) at the beginning of this year. Assume that

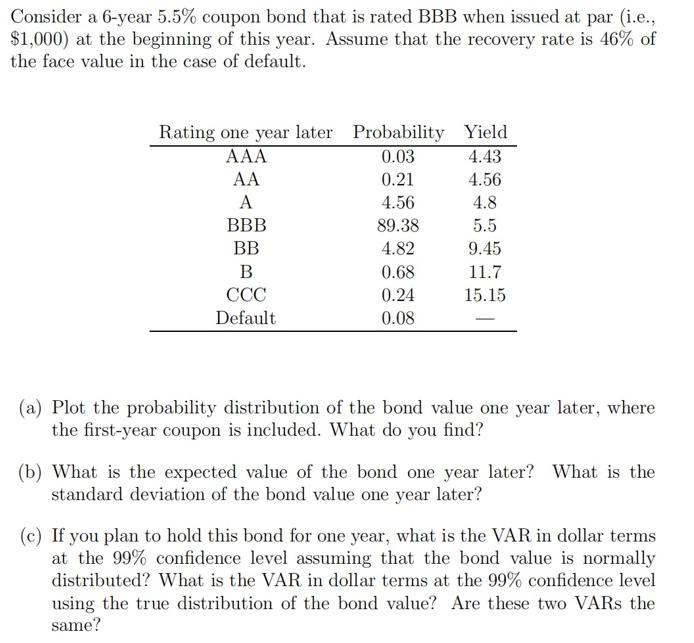

Consider a 6-year 5.5% coupon bond that is rated BBB when issued at par (i.e., $1,000) at the beginning of this year. Assume that the recovery rate is 46% of the face value in the case of default. Rating one year later Probability Yield 0.03 4.43 4.56 4.8 5.5 9.45 AAA AA A BBB BB B CCC Default 0.21 4.56 89.38 4.82 0.68 0.24 0.08 11.7 15.15 (a) Plot the probability distribution of the bond value one year later, where the first-year coupon is included. What do you find? (b) What is the expected value of the bond one year later? What is the standard deviation of the bond value one year later? (c) If you plan to hold this bond for one year, what is the VAR in dollar terms at the 99% confidence level assuming that the bond value is normally distributed? What is the VAR in dollar terms at the 99% confidence level using the true distribution of the bond value? Are these two VARs the same?

Step by Step Solution

3.49 Rating (142 Votes )

There are 3 Steps involved in it

a To plot the probability distribution of the bond value one year later we need to calculate the bond value under each rating scenario one year later ... View full answer

Get step-by-step solutions from verified subject matter experts