Question

Consider a European call option on a non-dividend-paying stock; when the option is written, the stock price is S 0 , the volatility of the

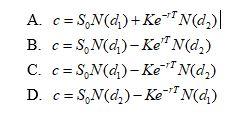

Consider a European call option on a non-dividend-paying stock; when the option is written, the stock price is S0, the volatility of the stock price is , the strike price is K, the continuously compounded risk-free rate is r, and the term to expiration is T; let c be the price of the option. The Black-Scholes formula for the option price is

where N(x) is the cumulative probability distribution function for a standardized normal distribution and d1 and d2 are parameters dependant on the structure of the option, the level of interest rates, and the volatility of the stock price.

13. (a) Using the terminology of the last question (re-printed above Question 8 from the multiple choice section), specify the Black-Scholes formula for the price of a European put option on a non-dividend-paying stock

(b) Explicitly describe the relationship of the parameters d1 and d2 to the structure of the option, the level of interest rates and the volatility of the stock price and the relationship of the parameters to each other; use the notation of the last question (e.g., write the formulas for d1 and d2 )

(c) We found that for a dividend yielding stock that there was a simple enhancement possible to convert the result in question 3) to the case of a European call option on a dividend yielding stock. Let q represent the dividend yield and describe the enhancement (which we found appropriate in many representations). Also, show the result for the European call option on a dividend yielding stock (include the formula for d1 and d2 ).

A. c = SN(d)+ Ke-N(d.) B. c = SN(d)-Ken(d,) C. c=SN(d)-Ke-'T N(d)) D. c = SN(d)-Ke-N(d)Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Healthcare Finance An Introduction To Accounting And Financial Management

Authors: Louis Gapenski PhD

3rd Edition

1567932320, 978-1567932324