Question

Consider a financial institution that enters into a foreign currency swap for which the institution receives 5.875 percent per annum semi-annually in French francs and

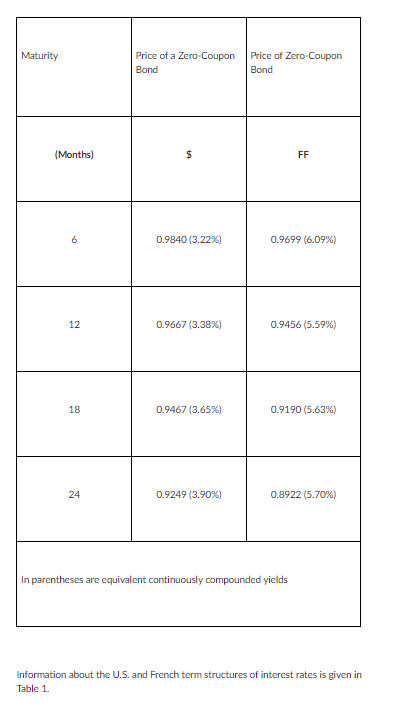

Consider a financial institution that enters into a foreign currency swap for which the institution receives 5.875 percent per annum semi-annually in French francs and pays 3.75 percent per annum semi-annually in U.S. dollars. The maturity of the swap is in two years and the current spot exchange rate is 0.20 U.S.$/FF. The principals in the two currencies are 58 million francs and 10 million dollars. Table 1 Domestic and Foreign Term Structure

What is the current value of the swap (in millions)?

Question 2 options:

| $1.000 m | |

| $2.300 m | |

| $1.654 m | |

| None of the above |

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Quantum Investing Unlocking The Secrets Of The New Financial System

Authors: Hugh Webb

1st Edition

979-8388948823