Answered step by step

Verified Expert Solution

Question

1 Approved Answer

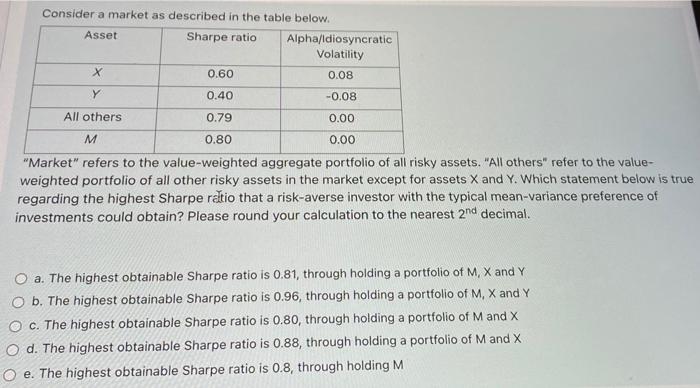

Consider a market as described in the table below. Asset Sharpe ratio Alpha/Idiosyncratic Volatility X 0.60 0.08 Y 0.40 -0.08 All others 0.79 0.00 M

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managing The Audit Function A Corporate Audit Department Procedures Guide

Authors: Michael P. Cangemi

2nd Edition

0471012556, 978-0471012559