Answered step by step

Verified Expert Solution

Question

1 Approved Answer

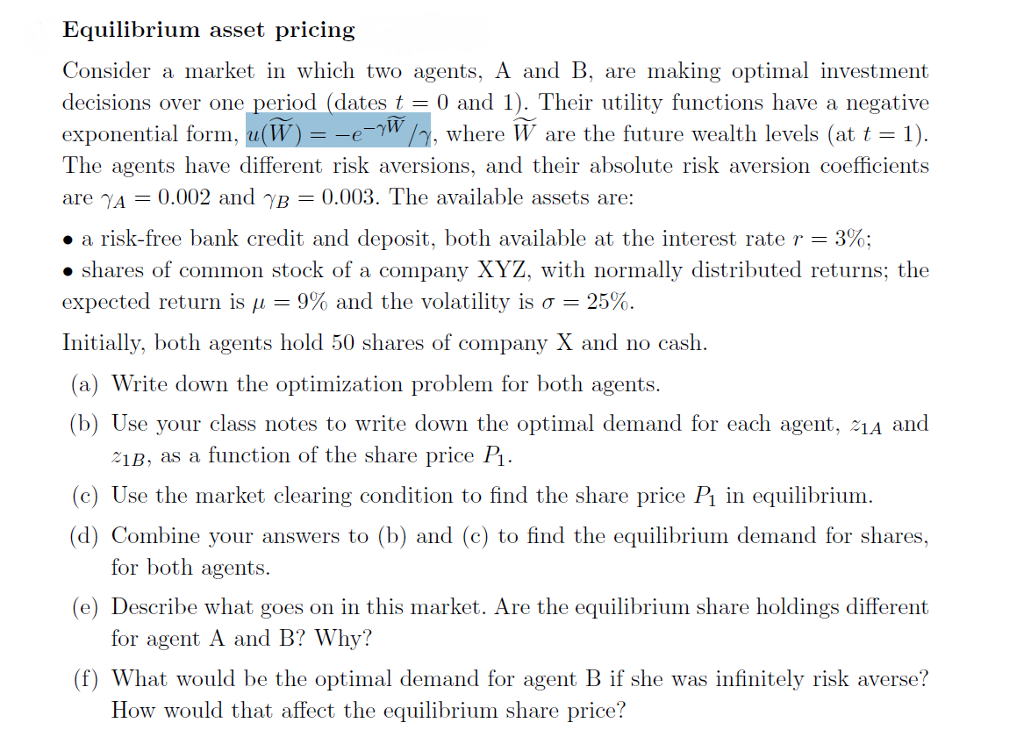

Consider a market in which two agents, A and B, are making optimal investment decisions over one period (dates t=0 and 1). Their utility functions

Consider a market in which two agents, A and B, are making optimal investment decisions over one period (dates t=0 and 1). Their utility functions have a negative potential.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Palgrave Macmillan Understanding Investment Funds Insights From Performance And Risk Analysis

Authors: V. Terraza , H. Razafitombo

1st Edition

1137273607,1137273615