Answered step by step

Verified Expert Solution

Question

1 Approved Answer

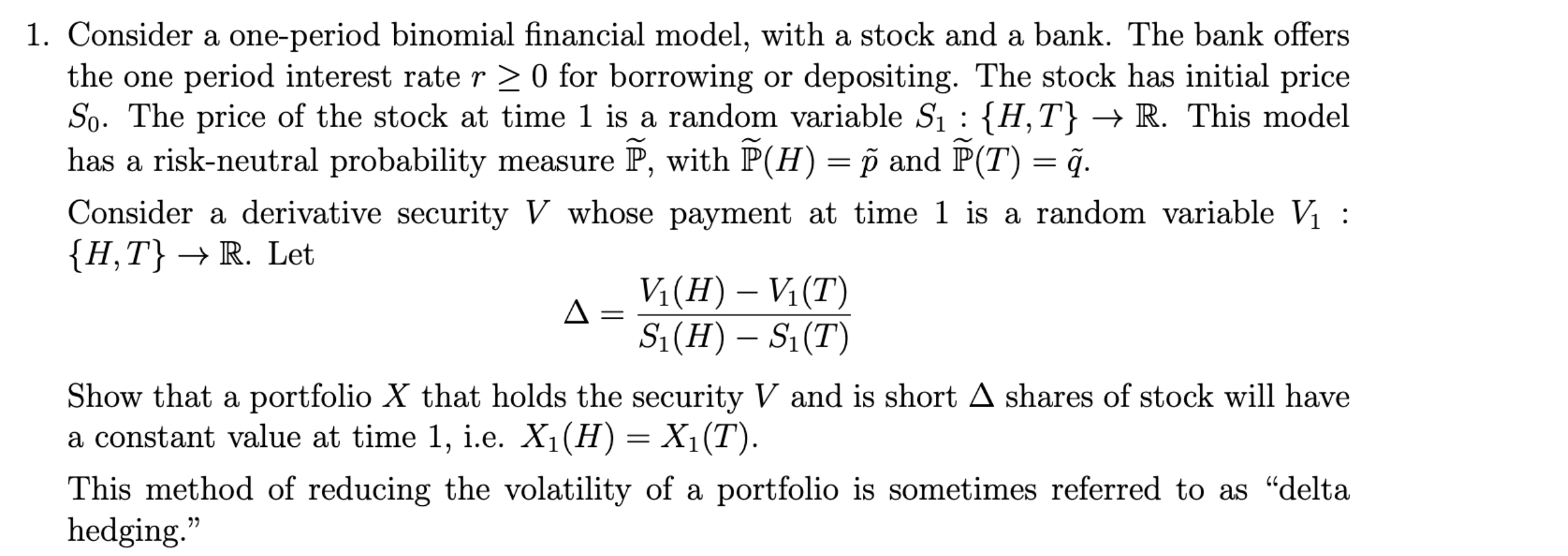

Consider a one - period binomial financial model, with a stock and a bank. The bank offers the one period interest rate r 0 for

Consider a oneperiod binomial financial model, with a stock and a bank. The bank offers

the one period interest rate for borrowing or depositing. The stock has initial price

The price of the stock at time is a random variable : This model

has a riskneutral probability measure widetilde with widetildetilde and widetildetilde

Consider a derivative security whose payment at time is a random variable :

Let

Show that a portfolio that holds the security and is short shares of stock will have

a constant value at time ie

This method of reducing the volatility of a portfolio is sometimes referred to as "delta

hedging."

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

All About Options

Authors: Thomas McCafferty

3rd Edition

0071484795, 978-0071484794