Answered step by step

Verified Expert Solution

Question

1 Approved Answer

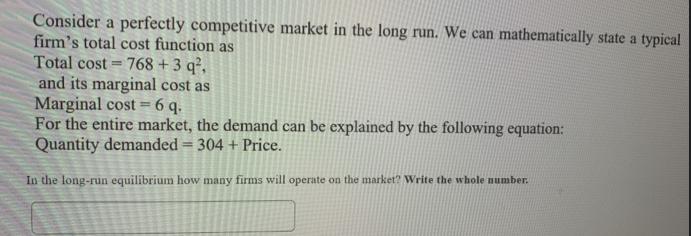

Consider a perfectly competitive market in the long run. We can mathematically state a typical firm's total cost function as Total cost 768 +3

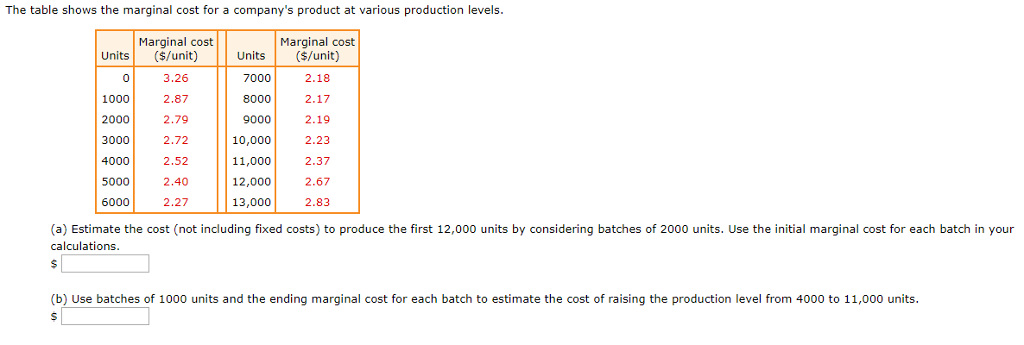

Consider a perfectly competitive market in the long run. We can mathematically state a typical firm's total cost function as Total cost 768 +3 q, and its marginal cost as Marginal cost = 6 q. For the entire market, the demand can be explained by the following equation: Quantity demanded = 304 + Price. In the long-run equilibrium how many firms will operate on the market? Write the whole number. The table shows the marginal cost for a company's product at various production levels. Marginal cost ($/unit) Marginal cost ($/unit) 3.26 2.18 2.87 2.17 2.79 2.19 2.72 2.23 2.52 2.37 2.40 2.67 2.27 2.83 Units 0 $ 1000 2000 3000 4000 5000 6000 Units 7000 8000 9000 10,000 11,000 12,000 13,000 (a) Estimate the cost (not including fixed costs) to produce the first 12,000 units by considering batches of 2000 units. Use the initial marginal cost for each batch in your calculations. (b) Use batches of 1000 units and the ending marginal cost for each batch to estimate the cost of raising the production level from 4000 to 11,000 units. S

Step by Step Solution

There are 3 Steps involved in it

Step: 1

a Estimating Cost with Batches of 2000 Units Heres how to estimate the cost to produce the first 120...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles of Economics

Authors: Gregory Mankiw

7th edition

128516587X, 978-1285165875