Answered step by step

Verified Expert Solution

Question

1 Approved Answer

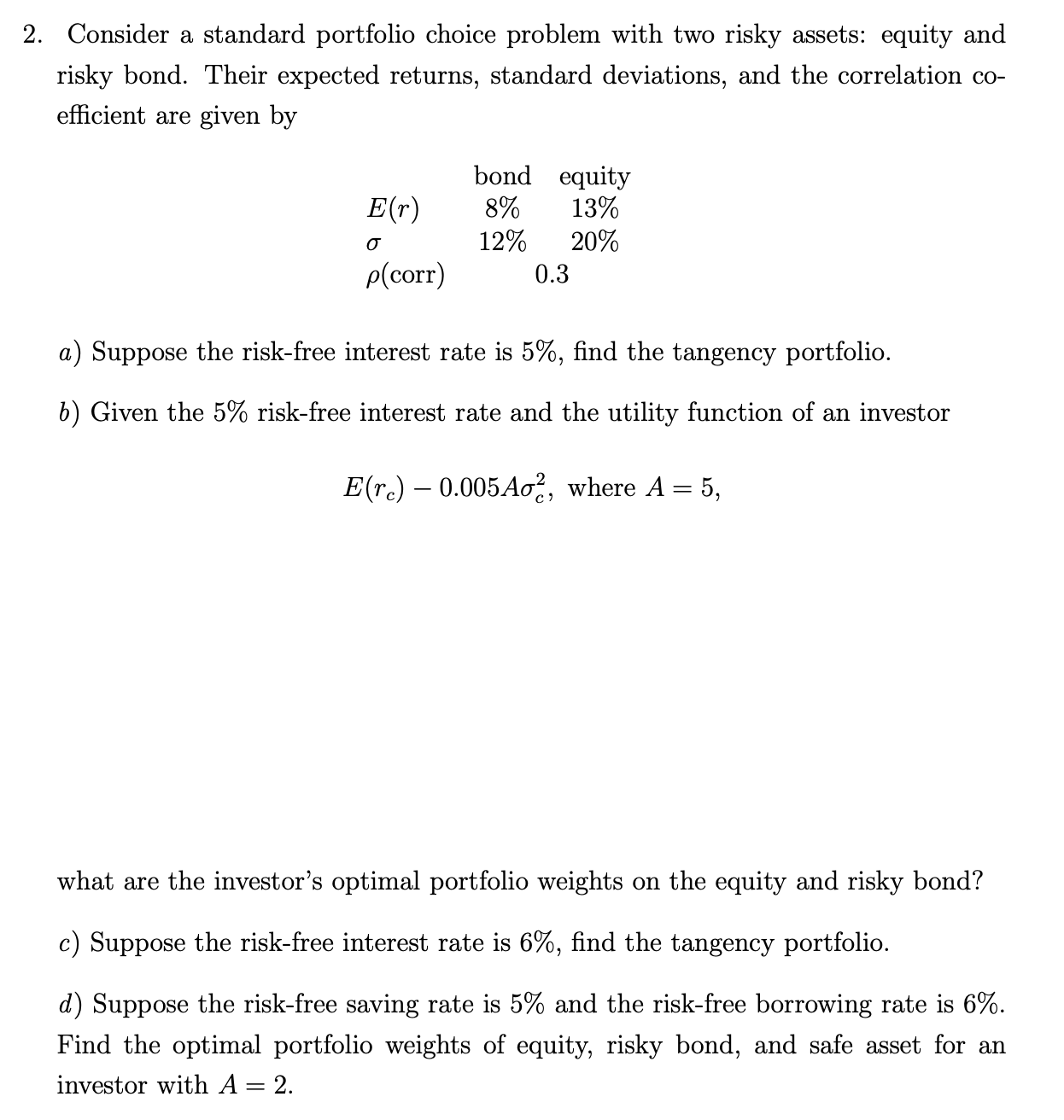

Consider a standard portfolio choice problem with two risky assets: equity and risky bond. Their expected returns, standard deviations, and the correlation co - efficient

Consider a standard portfolio choice problem with two risky assets: equity and

risky bond. Their expected returns, standard deviations, and the correlation co

efficient are given by

a Suppose the riskfree interest rate is find the tangency portfolio.

b Given the riskfree interest rate and the utility function of an investor

where

what are the investor's optimal portfolio weights on the equity and risky bond?

c Suppose the riskfree interest rate is find the tangency portfolio.

d Suppose the riskfree saving rate is and the riskfree borrowing rate is

Find the optimal portfolio weights of equity, risky bond, and safe asset for an

investor with

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Investments

Authors: William F. Sharpe, Gordon J. Alexander, Jeffery V. Bailey

6th Edition

8120321014, 978-8120321014