Question

Consider a two-stock portfolio consisting of 200 shares of KL Enterprises at $25/share and 100 shares of Sherman Inc. at $75/share. You also have the

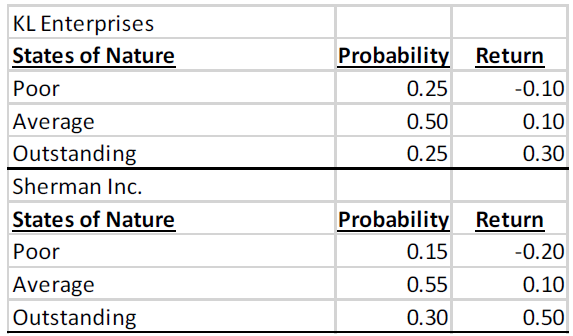

Consider a two-stock portfolio consisting of 200 shares of KL Enterprises at $25/share and 100 shares of Sherman Inc. at $75/share.

You also have the following data:

The correlation of the returns for KL and Sherman is 0.1. What is the expected return and standard deviation of each stock and of your portfolio?

KL Enterprises States of Nature Poor Average Outstanding Sherman Inc. Probability Return 0.25 -0.10 0.50 0.10 0.25 0.30 States of Nature Poor Probability Return 0.15 -0.20 0.55 0.10 0.30 0.50 Average Outstanding

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Optimization Methods In Finance

Authors: Gerard Cornuejols, Reha Tütüncü

1st Edition

0521861705, 978-0521861700