Answered step by step

Verified Expert Solution

Question

1 Approved Answer

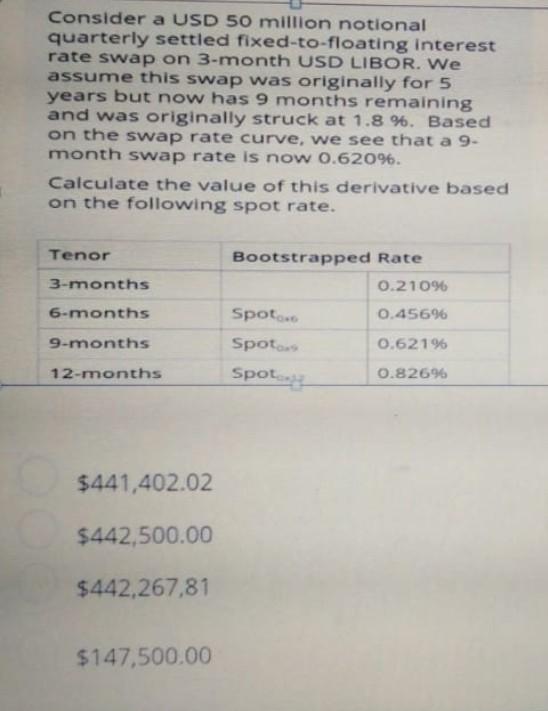

Consider a USD 50 million notional quarterly settled fixed-to-floating interest rate swap on 3-month USD LIBOR. We assume this swap was originally for 5 years

Consider a USD 50 million notional quarterly settled fixed-to-floating interest rate swap on 3-month USD LIBOR. We assume this swap was originally for 5 years but now has 9 months remaining and was originally struck at 1.8 %. Based on the swap rate curve, we see that a 9- month swap rate is now 0.62096. Calculate the value of this derivative based on the following spot rate. Tenor 3-months 6-months Bootstrapped Rate 0.210% Spot... 0.45696 Spot 0.621% 0.82696 9-months 12-months Spot $441,402.02 $442,500.00 $442,267,81 $147,500.00

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Oxford Handbook Of Hedge Funds

Authors: Douglas Cumming, Sofia Johan, Geoffrey Wood

1st Edition

0198840950, 978-0198840954