Answered step by step

Verified Expert Solution

Question

1 Approved Answer

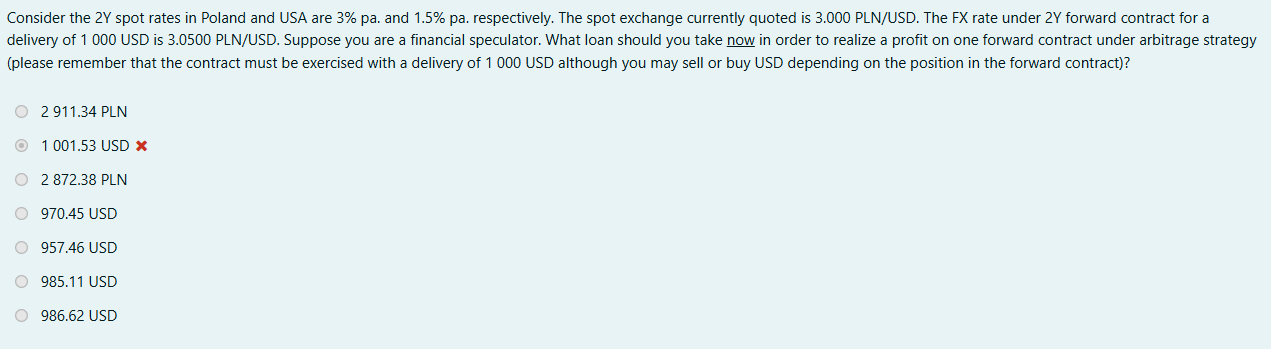

Consider the 2 Y spot rates in Poland and USA are 3 % pa . and 1 . 5 % pa . respectively. The spot

Consider the Y spot rates in Poland and USA are pa and pa respectively. The spot exchange currently quoted is The FX rate under Y forward contract for a delivery of USD is PLNUSD Suppose you are a financial speculator. What loan should you take now in order to realize a profit on one forward contract under arbitrage strategy

please remember that the contract must be exercised with a delivery of USD although you may sell or buy USD depending on the position in the forward contract

PLN

USD

PLN

USD

USD

USD

USD

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Risk Management In Forex How To Minimize Losses And Maximize Returns

Authors: Eunice Loar

1st Edition

979-8388778864