Answered step by step

Verified Expert Solution

Question

1 Approved Answer

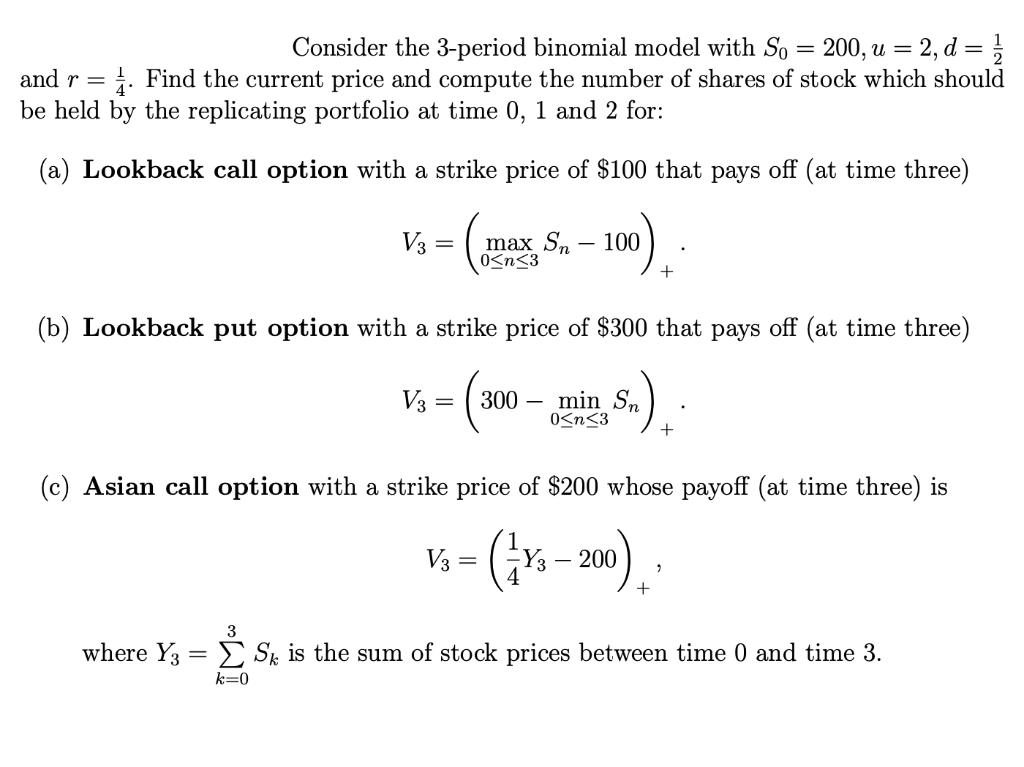

Consider the 3-period binomial model with So = 200, u = 2, d = // and r = Find the current price and compute

Consider the 3-period binomial model with So = 200, u = 2, d = // and r = Find the current price and compute the number of shares of stock which should be held by the replicating portfolio at time 0, 1 and 2 for: (a) Lookback call option with a strike price of $100 that pays off (at time three) 100) (b) Lookback put option with a strike price of $300 that pays off (at time three) where Y3 = 3 V3 k=0 = (c) Asian call option with a strike price of $200 whose payoff (at time three) is (Y-200) Y3 V3: = 300 - min Sn 0

Step by Step Solution

★★★★★

3.49 Rating (152 Votes )

There are 3 Steps involved in it

Step: 1

Lets draw the possible state of prices at the end of each period The table below summarises differen...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Intermediate Accounting

Authors: Elizabeth A. Gordon, Jana S. Raedy, Alexander J. Sannella

1st edition

978-0133251579, 133251578, 013216230X, 978-0134102313, 134102312, 978-0132162302