Answered step by step

Verified Expert Solution

Question

1 Approved Answer

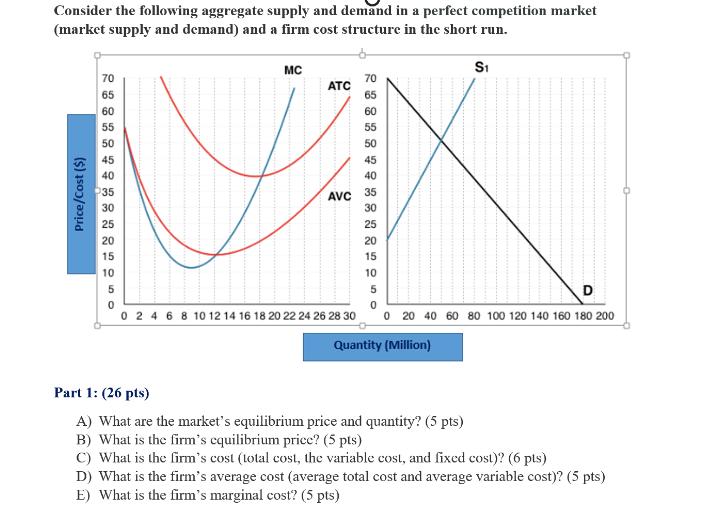

Consider the following aggregate supply and demand in a perfect competition market (market supply and demand) and a firm cost structure in the short

Consider the following aggregate supply and demand in a perfect competition market (market supply and demand) and a firm cost structure in the short run. MC 70 ATC 65 60 55 50 45 NK 40 35 AVC 30 25 20 15 10 5 0 0 20 40 60 80 100 120 140 160 180 200 70 65 60 55 50 45 40 35 30 25 20 15 10 5 0 0 2 4 6 8 10 12 14 16 18 20 22 24 26 28 30 Quantity (Million) S1 Part 1: (26 pts) A) What are the market's equilibrium price and quantity? (5 pts) B) What is the firm's equilibrium price? (5 pts) C) What is the firm's cost (total cost, the variable cost, and fixed cost)? (6 pts) D) What is the firm's average cost (average total cost and average variable cost)? (5 pts) E) What is the firm's marginal cost? (5 pts) Part 2: Suppose the price falls to $40. (24 pts) A) Calculate the firm's total cost, total revenue, and profit. (12 pts) B) Should the firm operate at the new price level? Why? (12 pts) Part 3: Determine the shutdown point and calculate the firm's profit. Should the firm stay in the market at the shutdown point? Why? (25 pts) Part 4: The firm's board of directors has decided to provide their services to additional customers. They have to set up a new infrastructure. The firm has a low initial cost for setting up this infrastructure. Can they take advantage of economies of scale to provide their services to additional customers? Why? (25 pts)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Part 1 A The markets equilibrium price and quantity are determined by the intersection of the market supply and demand curves From the graph it appears that the equilibrium price is 45 and the equilib...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Microeconomics

Authors: Dean S. Karlan, Jonathan J. Morduch

2nd edition

1259813337, 1259813339, 978-1259813337