Answered step by step

Verified Expert Solution

Question

1 Approved Answer

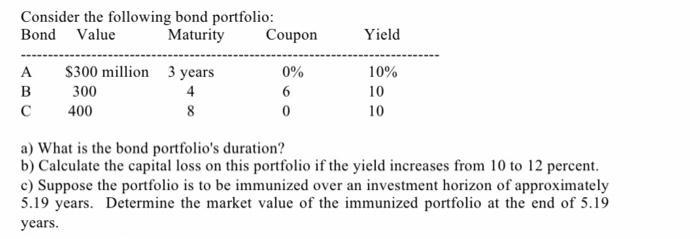

Consider the following bond portfolio: Bond Value Maturity A B $300 million 3 years 300 4 8 400 Coupon 0% 6 0 Yield 10%

Consider the following bond portfolio: Bond Value Maturity A B $300 million 3 years 300 4 8 400 Coupon 0% 6 0 Yield 10% 10 10 a) What is the bond portfolio's duration? b) Calculate the capital loss on this portfolio if the yield increases from 10 to 12 percent. c) Suppose the portfolio is to be immunized over an investment horizon of approximately 5.19 years. Determine the market value of the immunized portfolio at the end of 5.19 years.

Step by Step Solution

★★★★★

3.33 Rating (153 Votes )

There are 3 Steps involved in it

Step: 1

a The duration of a bond portfolio is calculated using the weighted average ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Income Tax Fundamentals 2013

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill

31st Edition

1111972516, 978-1285586618, 1285586611, 978-1285613109, 978-1111972516