Answered step by step

Verified Expert Solution

Question

1 Approved Answer

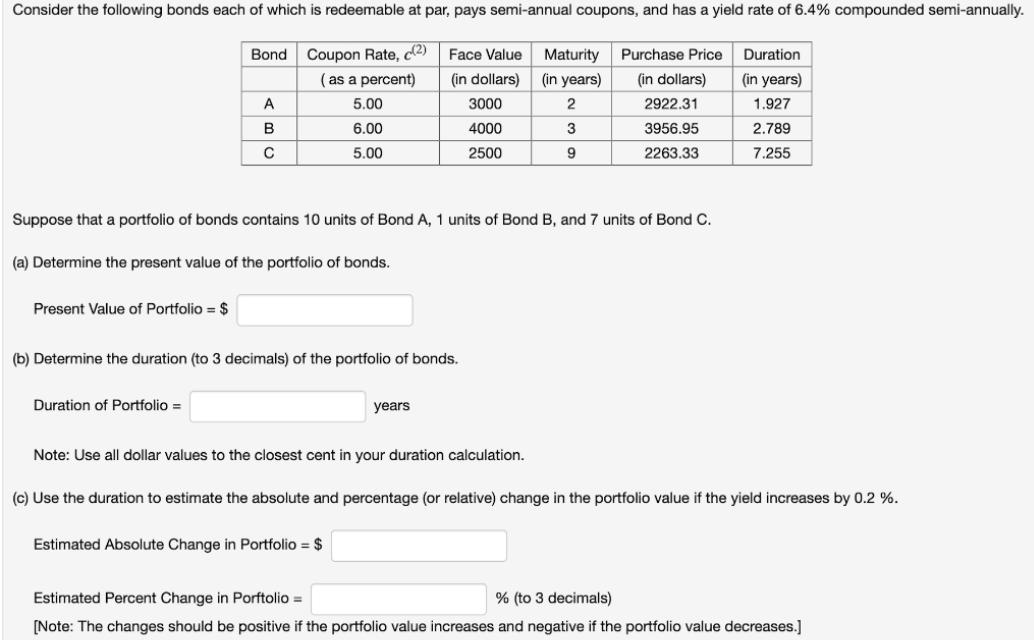

Consider the following bonds each of which is redeemable at par, pays semi-annual coupons, and has a yield rate of 6.4% compounded semi-annually. Coupon

Consider the following bonds each of which is redeemable at par, pays semi-annual coupons, and has a yield rate of 6.4% compounded semi-annually. Coupon Rate, c(2) (as a percent) 5.00 Present Value of Portfolio = $ Bond A B C Duration of Portfolio = 6.00 5.00 Suppose that a portfolio of bonds contains 10 units of Bond A, 1 units of Bond B, and 7 units of Bond C. (a) Determine the present value of the portfolio of bonds. (b) Determine the duration (to 3 decimals) of the portfolio of bonds. Face Value (in dollars) 3000 4000 2500 years Estimated Absolute Change in Portfolio = $ Note: Use all dollar values to the closest cent in your duration calculation. Maturity (in years) 2 3 9 Purchase Price (in dollars) 2922.31 3956.95 2263.33 Duration (in years) 1.927 2.789 7.255 (c) Use the duration to estimate the absolute and percentage (or relative) change in the portfolio value if the yield increases by 0.2 %. Estimated Percent Change in Porftolio= % (to 3 decimals) [Note: The changes should be positive if the portfolio value increases and negative if the portfolio value decreases.]

Step by Step Solution

There are 3 Steps involved in it

Step: 1

a Determine the present value of the portfolio of bonds For Bond A Coupon Rate 500 2 Face Value 3000 ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Management and Cost Accounting

Authors: Colin Drury

8th edition

978-1408041802, 1408041804, 978-1408048566, 1408048566, 978-1408093887