Answered step by step

Verified Expert Solution

Question

1 Approved Answer

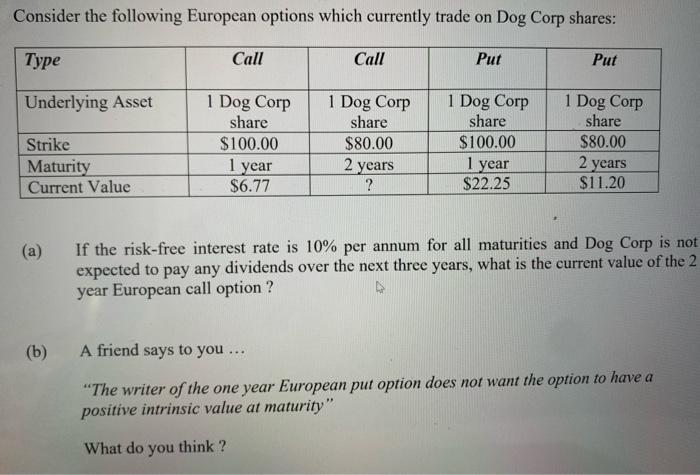

Consider the following European options which currently trade on Dog Corp shares: Put Type Call Call Put Underlying Asset 1 Dog Corp 1 Dog

Consider the following European options which currently trade on Dog Corp shares: Put Type Call Call Put Underlying Asset 1 Dog Corp 1 Dog Corp 1 Dog Corp 1 Dog Corp share share Strike $100.00 $80.00 share $100.00 share $80.00 Maturity 1 year 2 years 1 year 2 years Current Value $6.77 ? $22.25 $11.20 (a) (b) If the risk-free interest rate is 10% per annum for all maturities and Dog Corp is not expected to pay any dividends over the next three years, what is the current value of the 2 year European call option? A friend says to you... "The writer of the one year European put option does not want the option to have a positive intrinsic value at maturity" What do you think?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

a To calculate the current value of the 2year European call option we can use the BlackScholes for...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Foundations of Financial Management

Authors: Stanley Block, Geoffrey Hirt, Bartley Danielsen, Doug Short, Michael Perretta

10th Canadian edition

1259261018, 1259261015, 978-1259024979