Answered step by step

Verified Expert Solution

Question

1 Approved Answer

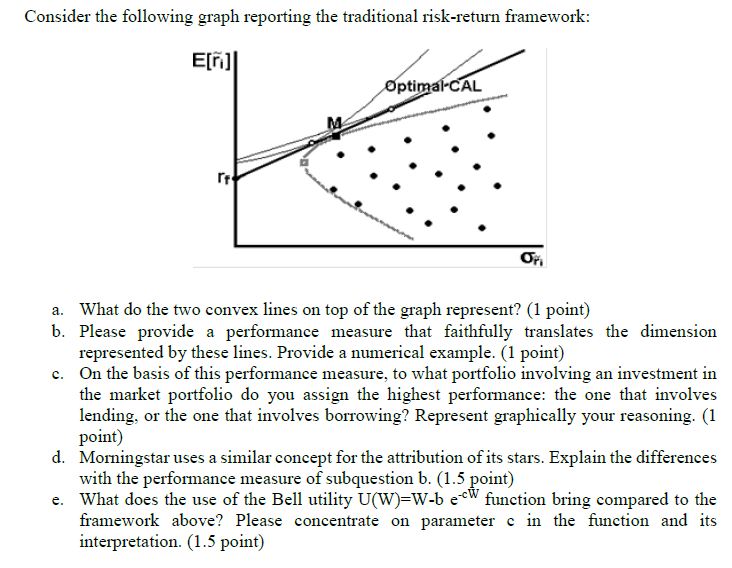

Consider the following graph reporting the traditional risk-return framework: E[n] rt Optimal-CAL Fi a. What do the two convex lines on top of the

Consider the following graph reporting the traditional risk-return framework: E[n] rt Optimal-CAL Fi a. What do the two convex lines on top of the graph represent? (1 point) b. Please provide a performance measure that faithfully translates the dimension represented by these lines. Provide a numerical example. (1 point) c. On the basis of this performance measure, to what portfolio involving an investment in the market portfolio do you assign the highest performance: the one that involves lending, or the one that involves borrowing? Represent graphically your reasoning. (1 point) d. Morningstar uses a similar concept for the attribution of its stars. Explain the differences with the performance measure of subquestion b. (1.5 point) e. What does the use of the Bell utility U(W)-W-b ew function bring compared to the framework above? Please concentrate on parameter c in the function and its interpretation. (1.5 point)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Chemical Principles

Authors: Steven S. Zumdahl, Donald J. DeCoste

7th edition

9781133109235, 1111580650, 978-1111580650