Answered step by step

Verified Expert Solution

Question

1 Approved Answer

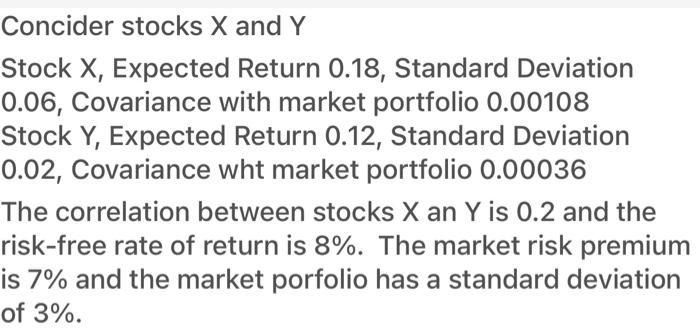

Consider the following information about two stocks X and Y. X's expected return 0.18, standard deviation 0.06, covariance with market portfolio 0.00108. Y's expected return

Consider the following information about two stocks X and Y. X's expected return 0.18, standard deviation 0.06, covariance with market portfolio 0.00108. Y's expected return 0.12, standard deviation 0.02, covariance eith market portfolio 0.00036.

a. Assume you combine the two stocks ina portfolio with thr goal to create an expected return of 15%. What proportion of your money should you invest in each of these stocks?

50%\50% 25%\75% 75%\25% 0%\100% 10%\90%

b.What is the standard deviation in an equally weighted portfolio between X and Y?

1.12% 3.35% 4.6% 13.78% 14.18%

c. what is the estimated lr empirical beta of an equally weighted protfolio between x and y

0.467? 0.8? 0.875? 1? 2?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Standards Of Value

Authors: Jay E. Fishman, Shannon P. Pratt, William J. Morrison

2nd Edition

1118138538, 978-1118138533