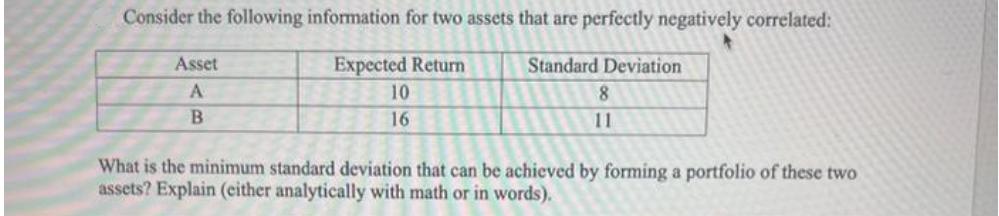

Question: Consider the following information for two assets that are perfectly negatively correlated: Expected Return Standard Deviation 10 16 Asset A B 8 What is

Consider the following information for two assets that are perfectly negatively correlated: Expected Return Standard Deviation 10 16 Asset A B 8 What is the minimum standard deviation that can be achieved by forming a portfolio of these two assets? Explain (either analytically with math or in words).

Step by Step Solution

★★★★★

3.52 Rating (165 Votes )

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

To determine the minimum standard deviation that can be achieved by forming a portfolio of two perfe... View full answer

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock