Answered step by step

Verified Expert Solution

Question

1 Approved Answer

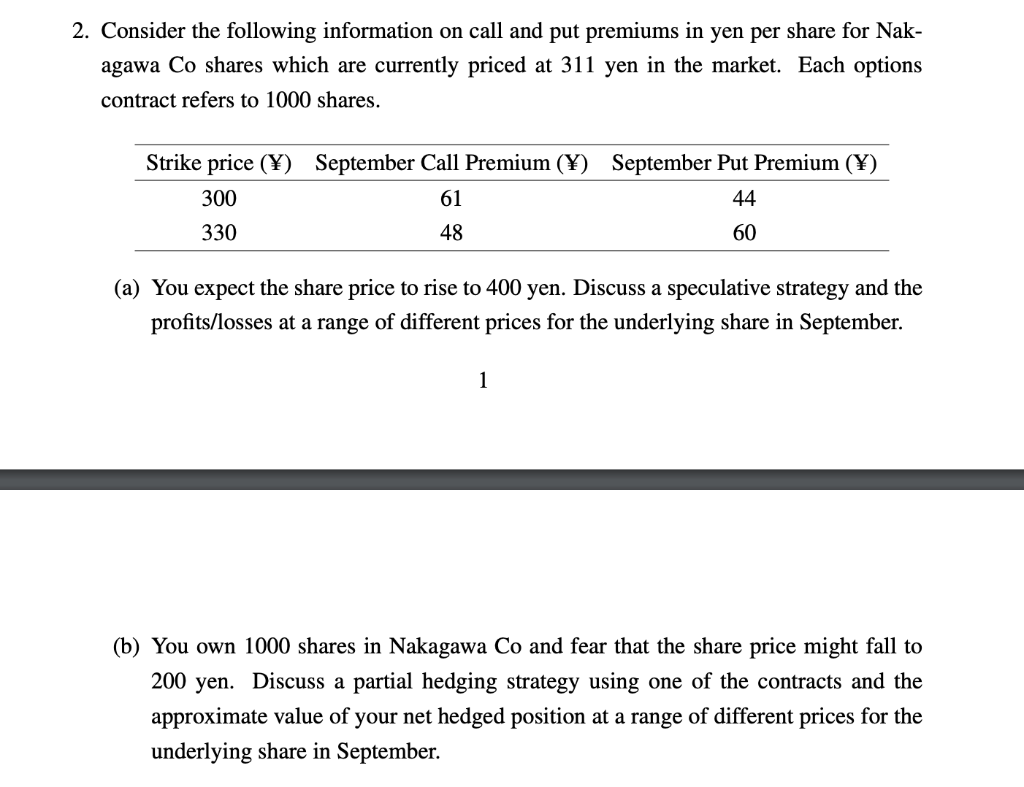

Consider the following information on call and put premiums in yen per share for Nakagawa Co shares which are currently priced at 311 yen in

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Take Charge Of Your Money Now Essential Strategies For Winning In Any Financial Climate

Authors: A.J. Monte, Rick Swope

1st Edition

0345517334, 978-0345517333