Answered step by step

Verified Expert Solution

Question

1 Approved Answer

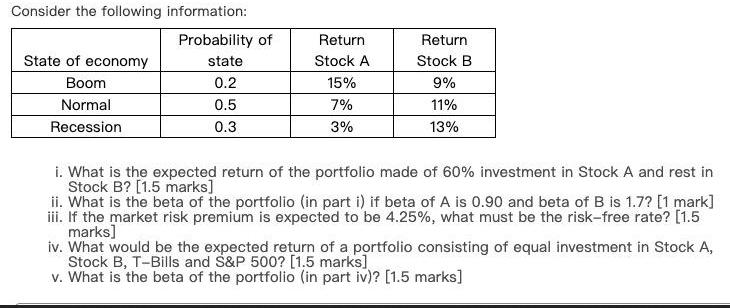

Consider the following information: Probability of Return Return State of economy state Stock A Stock B Boom 0.2 15% 9% Normal 0.5 7% 11%

Consider the following information: Probability of Return Return State of economy state Stock A Stock B Boom 0.2 15% 9% Normal 0.5 7% 11% Recession 0.3 3% 13% i. What is the expected return of the portfolio made of 60% investment in Stock A and rest in Stock B? [1.5 marks] ii. What is the beta of the portfolio (in part i) if beta of A is 0.90 and beta of B is 1.7? [1 mark] iii. If the market risk premium is expected to be 4.25%, what must be the risk-free rate? [1.5 marks] iv. What would be the expected return of a portfolio consisting of equal investment in Stock A, Stock B, T-Bills and S&P 500? [1.5 marks] v. What is the beta of the portfolio (in part iv)? [1.5 marks]

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Corporate Finance Core Principles and Applications

Authors: Stephen Ross, Randolph Westerfield, Jeffrey Jaffe, Bradford Jordan

5th edition

1259289907, 978-1259289903