Answered step by step

Verified Expert Solution

Question

1 Approved Answer

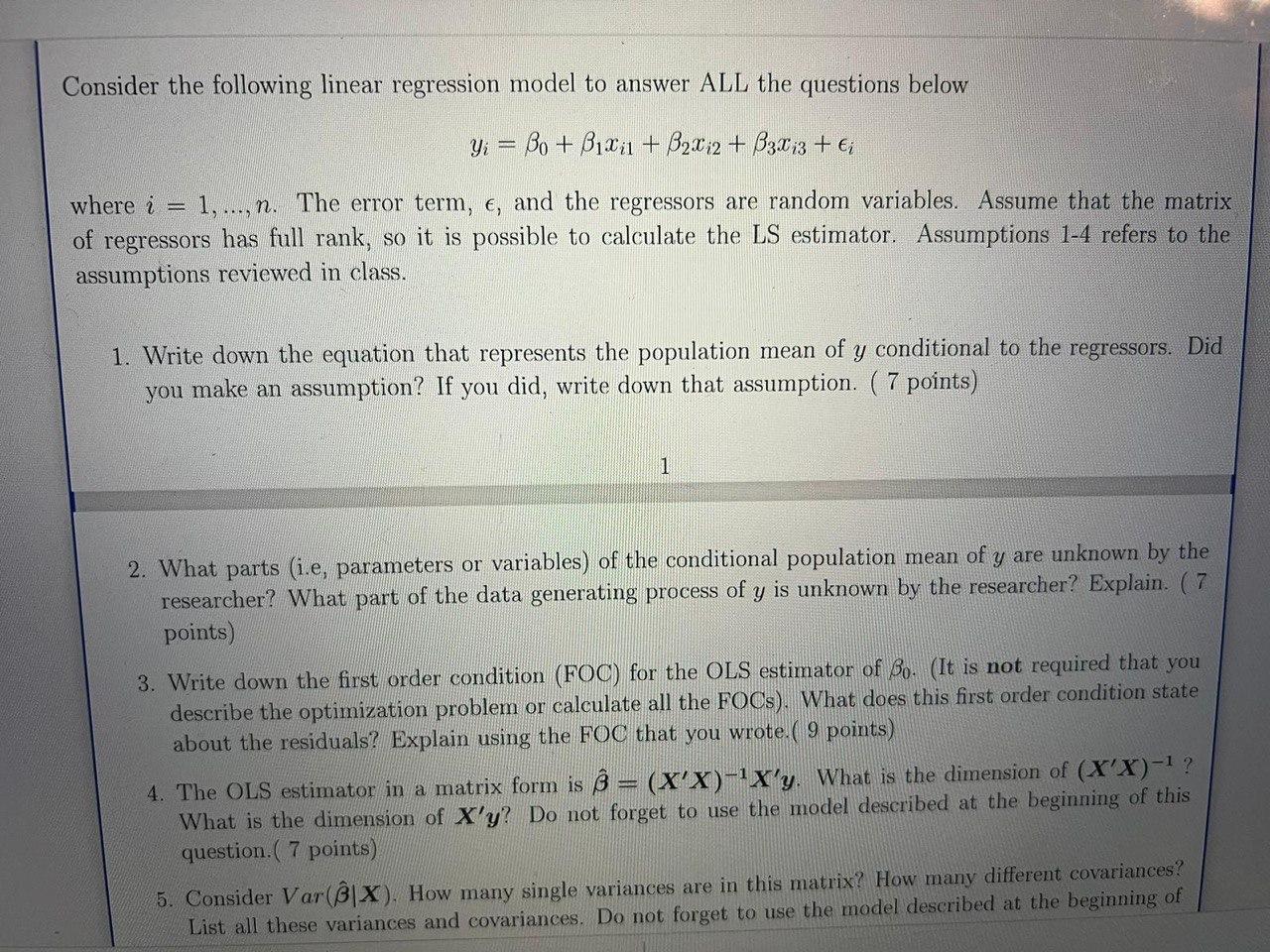

Consider the following linear regression model to answer ALL the questions below Yi = Bo+B1x1 + B2x12 + B3x13 + i where i =

Consider the following linear regression model to answer ALL the questions below Yi = Bo+B1x1 + B2x12 + B3x13 + i where i = 1,..., ,..., n. The error term, e, and the regressors are random variables. Assume that the matrix of regressors has full rank, so it is possible to calculate the LS estimator. Assumptions 1-4 refers to the assumptions reviewed in class. 1. Write down the equation that represents the population mean of y conditional to the regressors. Did you make an assumption? If you did, write down that assumption. (7 points) 1 2. What parts (i.e, parameters or variables) of the conditional population mean of y are unknown by the researcher? What part of the data generating process of y is unknown by the researcher? Explain. (7 points) 3. Write down the first order condition (FOC) for the OLS estimator of Bo. (It is not required that you describe the optimization problem or calculate all the FOCs). What does this first order condition state about the residuals? Explain using the FOC that you wrote.( 9 points) 4. The OLS estimator in a matrix form is = (X'X)-X'y. What is the dimension of (X'X)-? What is the dimension of X'y? Do not forget to use the model described at the beginning of this question.( 7 points) 5. Consider Var(BIX). How many single variances are in this matrix? How many different covariances? List all these variances and covariances. Do not forget to use the model described at the beginning of

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles of Financial Accounting

Authors: Belverd E. Needles, Marian Powers

12th edition

978-1133940562, 1133940560, 978-1285608464, 1285608461, 1133939287, 978-0357693605, 978-1285607047, 128560704X, 978-1133939283