Answered step by step

Verified Expert Solution

Question

1 Approved Answer

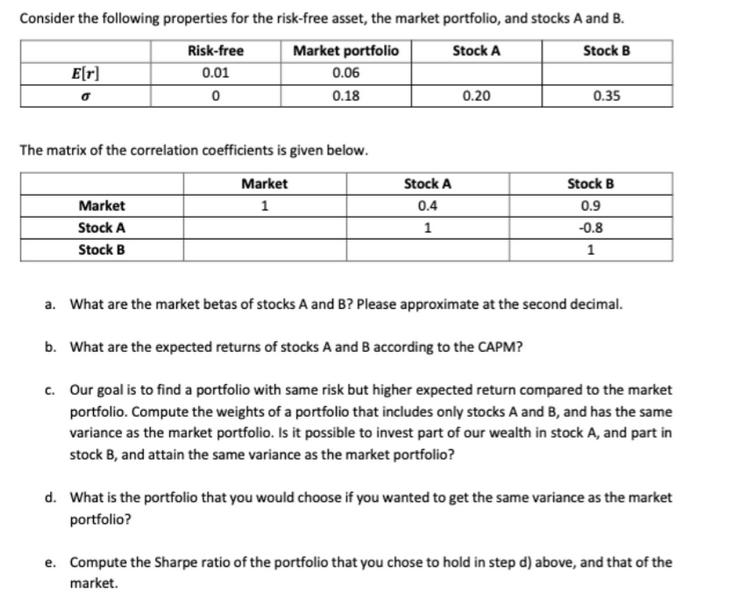

Consider the following properties for the risk-free asset, the market portfolio, and stocks A and B. E[r] Risk-free 0.01 0 Market portfolio 0.06 0.18

Consider the following properties for the risk-free asset, the market portfolio, and stocks A and B. E[r] Risk-free 0.01 0 Market portfolio 0.06 0.18 The matrix of the correlation coefficients is given below. Market Stock A Stock B Market 1 Stock A Stock B 0.20 0.35 Stock A 0.4 Stock B 0.9 1 -0.8 1 a. What are the market betas of stocks A and B? Please approximate at the second decimal. b. What are the expected returns of stocks A and B according to the CAPM? c. Our goal is to find a portfolio with same risk but higher expected return compared to the market portfolio. Compute the weights of a portfolio that includes only stocks A and B, and has the same variance as the market portfolio. Is it possible to invest part of our wealth in stock A, and part in stock B, and attain the same variance as the market portfolio? d. What is the portfolio that you would choose if you wanted to get the same variance as the market portfolio? e. Compute the Sharpe ratio of the portfolio that you chose to hold in step d) above, and that of the market.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Understanding Basic Statistics

Authors: Charles Henry Brase, Corrinne Pellillo Brase

6th Edition

978-1133525097, 1133525091, 1111827028, 978-1133110316, 1133110312, 978-1111827021