Answered step by step

Verified Expert Solution

Question

1 Approved Answer

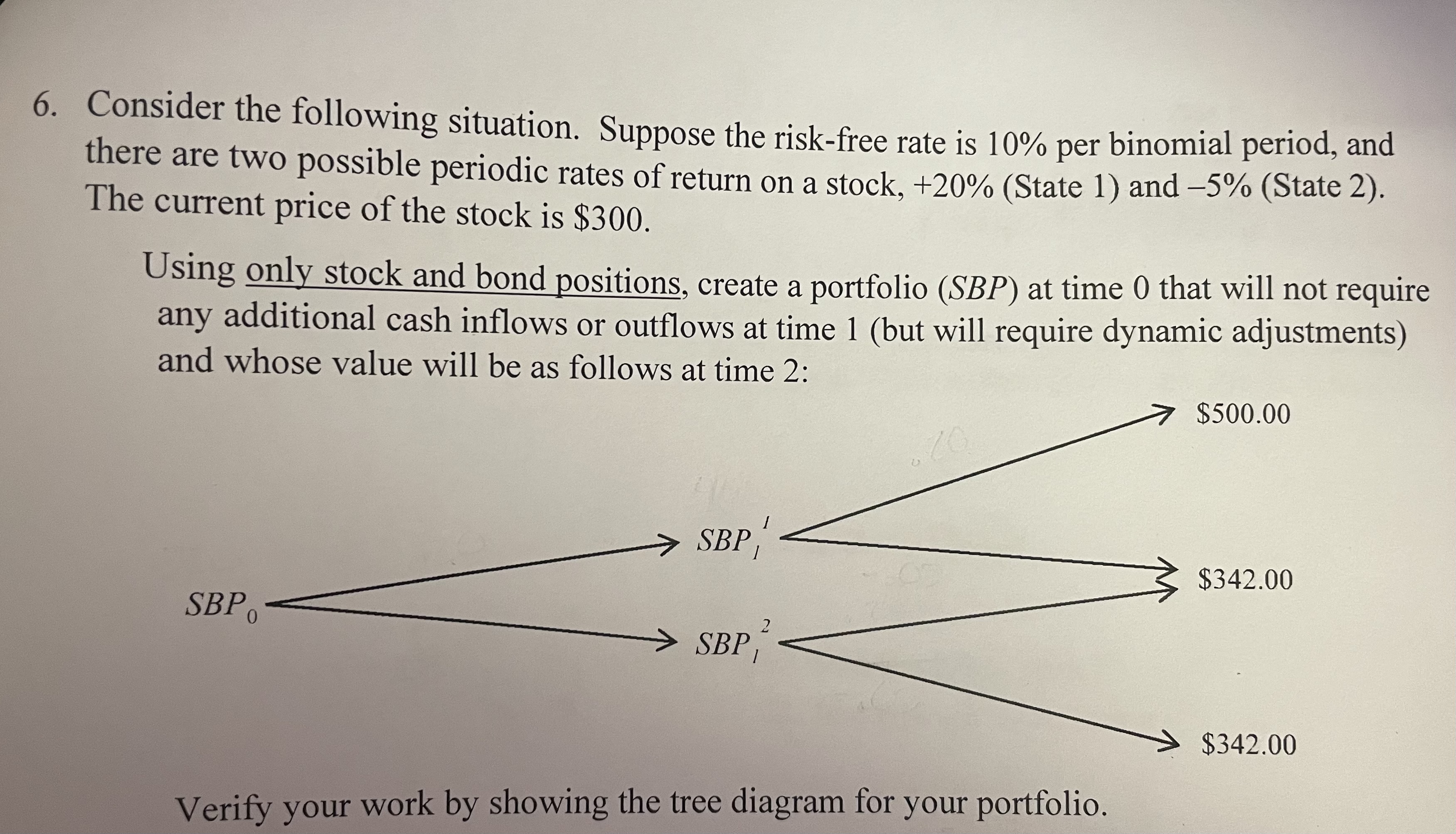

Consider the following situation. Suppose the risk-free rate is 10% per binomial period, and there are two possible periodic rates of return on a stock,

Consider the following situation. Suppose the risk-free rate is 10% per binomial period, and there are two possible periodic rates of return on a stock, +20% (State 1 ) and 5% (State 2 ). The current price of the stock is $300. Using only stock and bond positions, create a portfolio (SBP) at time 0 that will not require any additional cash inflows or outflows at time 1 (but will require dynamic adjustments) and whose value will be as follows at time 2 : Verify your work by showing the tree diagram for your portfolio

Consider the following situation. Suppose the risk-free rate is 10% per binomial period, and there are two possible periodic rates of return on a stock, +20% (State 1 ) and 5% (State 2 ). The current price of the stock is $300. Using only stock and bond positions, create a portfolio (SBP) at time 0 that will not require any additional cash inflows or outflows at time 1 (but will require dynamic adjustments) and whose value will be as follows at time 2 : Verify your work by showing the tree diagram for your portfolio Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Legal Handbook For Financial Planning In 2019

Authors: Allen Buckley

1st Edition

1091578826, 978-1091578821