Answered step by step

Verified Expert Solution

Question

1 Approved Answer

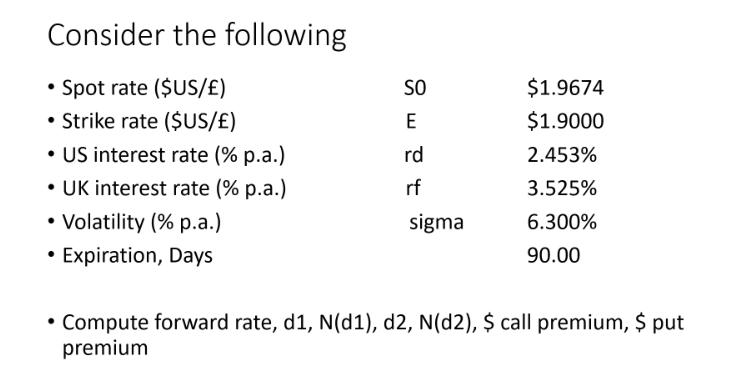

Consider the following Spot rate ($US/) Strike rate ($US/E) US interest rate (% p.a.) UK interest rate (% p.a.) Volatility (% p.a.) Expiration, Days

Consider the following Spot rate ($US/) Strike rate ($US/E) US interest rate (% p.a.) UK interest rate (% p.a.) Volatility (% p.a.) Expiration, Days SO E rd rf sigma $1.9674 $1.9000 2.453% 3.525% 6.300% 90.00 Compute forward rate, d1, N(d1), d2, N(d2), $ call premium, $ put premium

Step by Step Solution

★★★★★

3.52 Rating (169 Votes )

There are 3 Steps involved in it

Step: 1

To compute the forward rate d1 Nd1 d2 Nd2 call premium and put premium we need to use the BlackSchol...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

International Financial Management

Authors: Geert Bekaert, Robert J. Hodrick

2nd edition

013299755X, 132162768, 9780132997553, 978-0132162760