Question

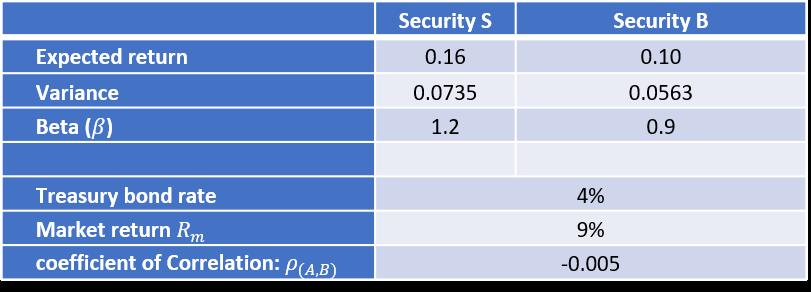

Consider the following two risky asset worlds: Answer the following questions: a. Explain why the risk of any portfolio composed of (S) and (B) is

Answer the following questions:

a. Explain why the risk of any portfolio composed of (S) and (B) is less than weighted average risk of the two securities.

b. Calculate the expected return and the variance of a portfolio composed of (60%: S, 40%: B).

c. If the minimum variance portfolio of the two securities is (43.41%: S, 56.59%: B), what is the expected return and the variance of this portfolio?

d. Explain Why the risk of any portfolio composed of S and B is greater than the risk of the portfolio in question.

e. Use the CAPM to evaluate the expected return of the two security (S).

f. Explain why the expected return calculated in question 5 equals to the market return if beta equals 1.

Expected return Variance Beta (3) Treasury bond rate Market return Rm coefficient of Correlation: P(A,B) Security S 0.16 0.0735 1.2 Security B 0.10 4% 9% -0.005 0.0563 0.9

Step by Step Solution

3.42 Rating (146 Votes )

There are 3 Steps involved in it

Step: 1

a The risk of a portfolio composed of securities S and B is less than the weighted average risk of the two securities because the correlation between ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Data Analysis And Decision Making

Authors: Christian Albright, Wayne Winston, Christopher Zappe

4th Edition

538476125, 978-0538476126