Answered step by step

Verified Expert Solution

Question

1 Approved Answer

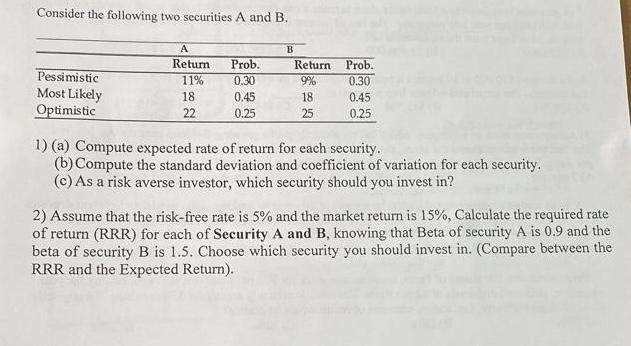

Consider the following two securities A and B. A B Return Prob. Return Prob. Pessimistic 11% 0.30 9% 0.30 Most Likely 18 0.45 18

Consider the following two securities A and B. A B Return Prob. Return Prob. Pessimistic 11% 0.30 9% 0.30 Most Likely 18 0.45 18 0.45 Optimistic 22 0.25 25 0.25 1) (a) Compute expected rate of return for each security. (b) Compute the standard deviation and coefficient of variation for each security. (c) As a risk averse investor, which security should you invest in? 2) Assume that the risk-free rate is 5% and the market return is 15%, Calculate the required rate of return (RRR) for each of Security A and B, knowing that Beta of security A is 0.9 and the beta of security B is 1.5. Choose which security you should invest in. (Compare between the RRR and the Expected Return).

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Income Tax Fundamentals 2013

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill

31st Edition

1111972516, 978-1285586618, 1285586611, 978-1285613109, 978-1111972516