Question

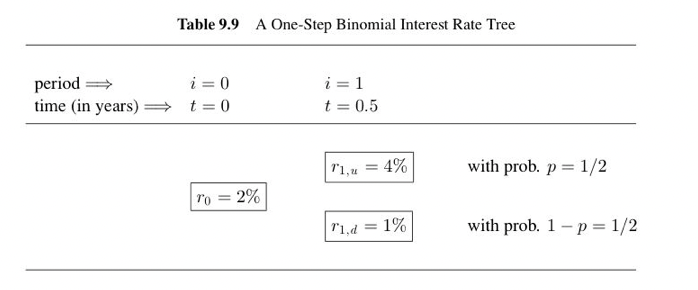

Consider the interest rate tree in Table 9.9. (a) Compute the expected 6-month Treasury rate E[r1 ]. (b) The 1-year Treasury bill is trading at

Consider the interest rate tree in Table 9.9. (a) Compute the expected 6-month Treasury rate E[r1 ]. (b) The 1-year Treasury bill is trading at P0 (2) = 97.4845. What is the (continu- ously compounded) forward rate for the periods i = 1 to i = 2? How does it compare with the expected rate computed in Part (a)? Explain. (c) Compute the market price of risk . Interpret. (d) Compute the risk neutral probability p . Interpret.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Secret Language Of Money How To Make Smarter Financial Decisions And Live A Richer Life

Authors: David Krueger, John David Mann

1st Edition

0071623396,007171314X