Answered step by step

Verified Expert Solution

Question

1 Approved Answer

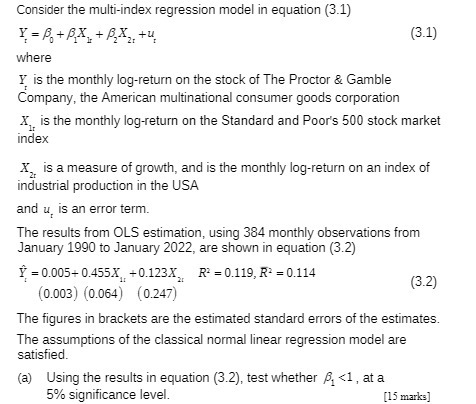

Consider the multi-index regression model in equation (3.1) Y = B+X+X+u where Y is the monthly log-return on the stock of The Proctor &

Consider the multi-index regression model in equation (3.1) Y = B+X+X+u where Y is the monthly log-return on the stock of The Proctor & Gamble Company, the American multinational consumer goods corporation (3.1) Xis the monthly log-return on the Standard and Poor's 500 stock market index X, is a measure of growth, and is the monthly log-return on an index of industrial production in the USA and u, is an error term. The results from OLS estimation, using 384 monthly observations from January 1990 to January 2022, are shown in equation (3.2) =0.005+0.455X+0.123X R2 = 0.119, R = 0.114 (0.003) (0.064) (0.247) (3.2) The figures in brackets are the estimated standard errors of the estimates. The assumptions of the classical normal linear regression model are satisfied. (a) Using the results in equation (3.2), test whether B

Step by Step Solution

★★★★★

3.36 Rating (146 Votes )

There are 3 Steps involved in it

Step: 1

To test whether the coefficient 1 is less than 1 in the multiindex regression model we use the resul...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

A Pathway To Introductory Statistics

Authors: Jay Lehmann

1st Edition

0134107179, 978-0134107172