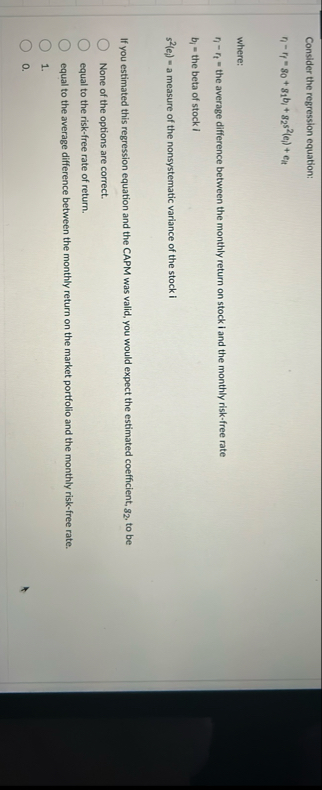

Question: Consider the regression equation: r 7 - r f = g 0 g 1 b i g 2 s 2 ( e i ) e

Consider the regression equation:

where:

the average difference between the monthly return on stock i and the monthly riskfree rate

the beta of stock I

a measure of the nonsystematic variance of the stock

If you estimated this regression equation and the CAPM was valid, you would expect the estimated coefficient, to be

None of the options are correct.

equal to the riskfree rate of return.

equal to the average difference between the monthly return on the market portfolio and the monthly riskfree rate.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock