Answered step by step

Verified Expert Solution

Question

1 Approved Answer

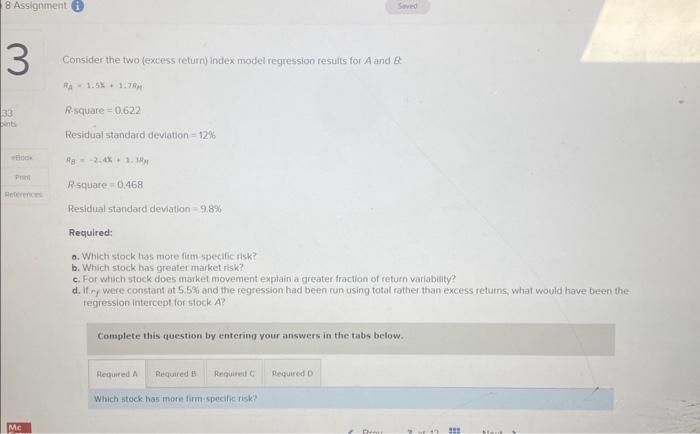

Consider the two (excess return) index model regression results for A and B. RA1.5K+1.7ThR-square=0.622Residualstandarddeviation=12% Residual standard deviation =12% Pg=2.4x+3.38H Rsquare =0.468 Residual standard devation =9.8%

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Digital Finance Bits And Bytes The Road Ahead

Authors: Vasant Chintaman Joshi

1st Edition