Answered step by step

Verified Expert Solution

Question

1 Approved Answer

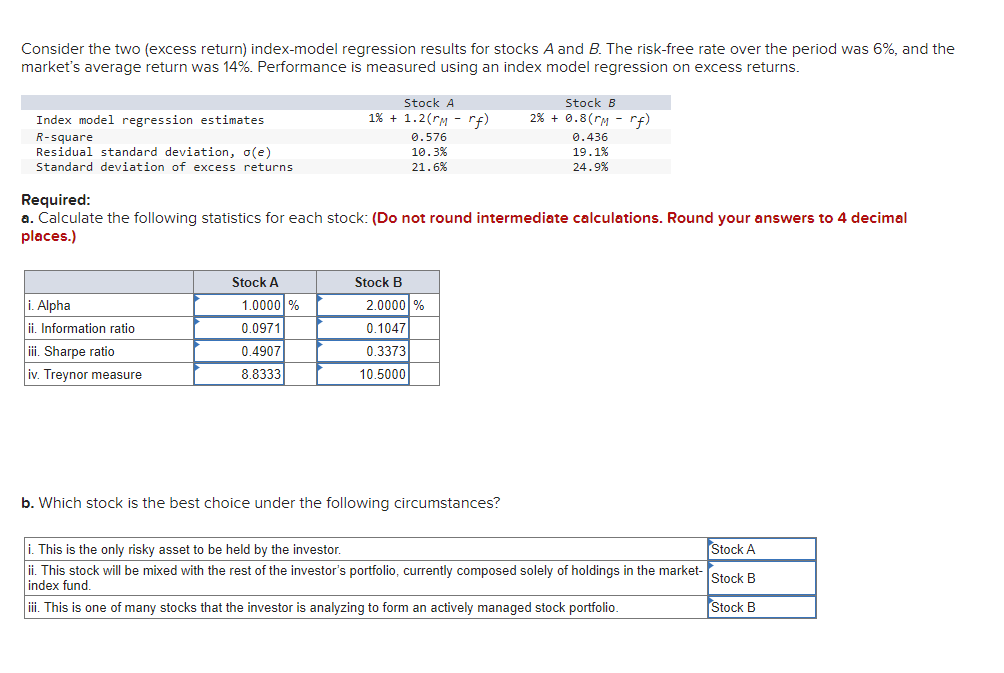

Consider the two (excess return) index-model regression results for stocks A and B. The risk-free rate over the period was 6%, and the market's average

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Handbook Of The Economics Of Corporate Governance Volume 1

Authors: Benjamin Hermalin , Michael Weisbach

1st Edition

0444635300,0444635408