Answered step by step

Verified Expert Solution

Question

1 Approved Answer

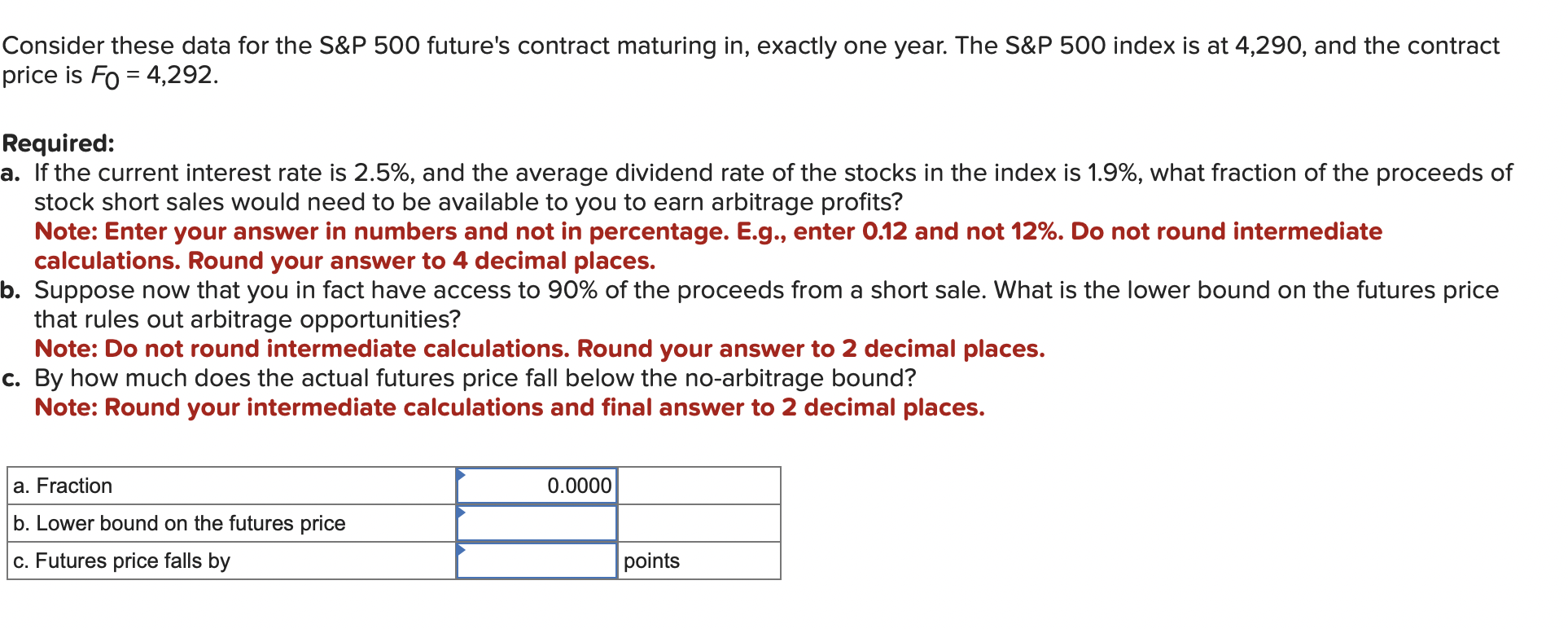

Consider these data for the S&P 500 future's contract maturing in, exactly one year. The S&P 500 index is at 4,290, and the contract price

Consider these data for the S\&P 500 future's contract maturing in, exactly one year. The S\&P 500 index is at 4,290, and the contract price is F0=4,292. Required: a. If the current interest rate is 2.5%, and the average dividend rate of the stocks in the index is 1.9%, what fraction of the proceeds of stock short sales would need to be available to you to earn arbitrage profits? Note: Enter your answer in numbers and not in percentage. E.g., enter 0.12 and not 12%. Do not round intermediate calculations. Round your answer to 4 decimal places. b. Suppose now that you in fact have access to 90% of the proceeds from a short sale. What is the lower bound on the futures price that rules out arbitrage opportunities? Note: Do not round intermediate calculations. Round your answer to 2 decimal places. c. By how much does the actual futures price fall below the no-arbitrage bound? Note: Round your intermediate calculations and final answer to 2 decimal places

Consider these data for the S\&P 500 future's contract maturing in, exactly one year. The S\&P 500 index is at 4,290, and the contract price is F0=4,292. Required: a. If the current interest rate is 2.5%, and the average dividend rate of the stocks in the index is 1.9%, what fraction of the proceeds of stock short sales would need to be available to you to earn arbitrage profits? Note: Enter your answer in numbers and not in percentage. E.g., enter 0.12 and not 12%. Do not round intermediate calculations. Round your answer to 4 decimal places. b. Suppose now that you in fact have access to 90% of the proceeds from a short sale. What is the lower bound on the futures price that rules out arbitrage opportunities? Note: Do not round intermediate calculations. Round your answer to 2 decimal places. c. By how much does the actual futures price fall below the no-arbitrage bound? Note: Round your intermediate calculations and final answer to 2 decimal places Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Teaching Public Budgeting And Finance

Authors: Meagan M. Jordan, Bruce D. McDonald III

1st Edition

1032146680, 978-1032146683