Answered step by step

Verified Expert Solution

Question

1 Approved Answer

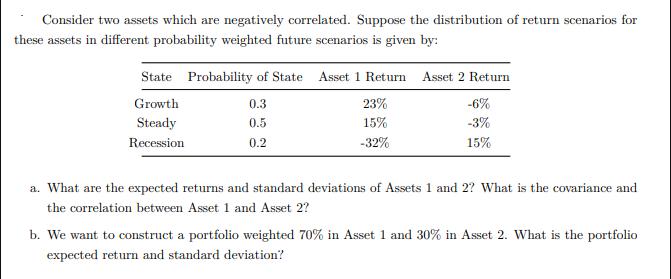

Consider two assets which are negatively correlated. Suppose the distribution of return scenarios for these assets in different probability weighted future scenarios is given

Consider two assets which are negatively correlated. Suppose the distribution of return scenarios for these assets in different probability weighted future scenarios is given by: State Probability of State Asset 1 Return Asset 2 Return Growth Steady Recession 0.3 0.5 0.2 23% 15% -32% -6% -3% 15% a. What are the expected returns and standard deviations of Assets 1 and 2? What is the covariance and the correlation between Asset 1 and Asset 2? b. We want to construct a portfolio weighted 70% in Asset 1 and 30% in Asset 2. What is the portfolio expected return and standard deviation?

Step by Step Solution

★★★★★

3.32 Rating (179 Votes )

There are 3 Steps involved in it

Step: 1

a To calculate the expected returns and standard deviations of Assets 1 and 2 as well as the covariance and correlation between them we can use the pr...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managerial Accounting An Integrative Approach

Authors: C J Mcnair Connoly, Kenneth Merchant

2nd Edition

099950049X, 978-0999500491