Answered step by step

Verified Expert Solution

Question

1 Approved Answer

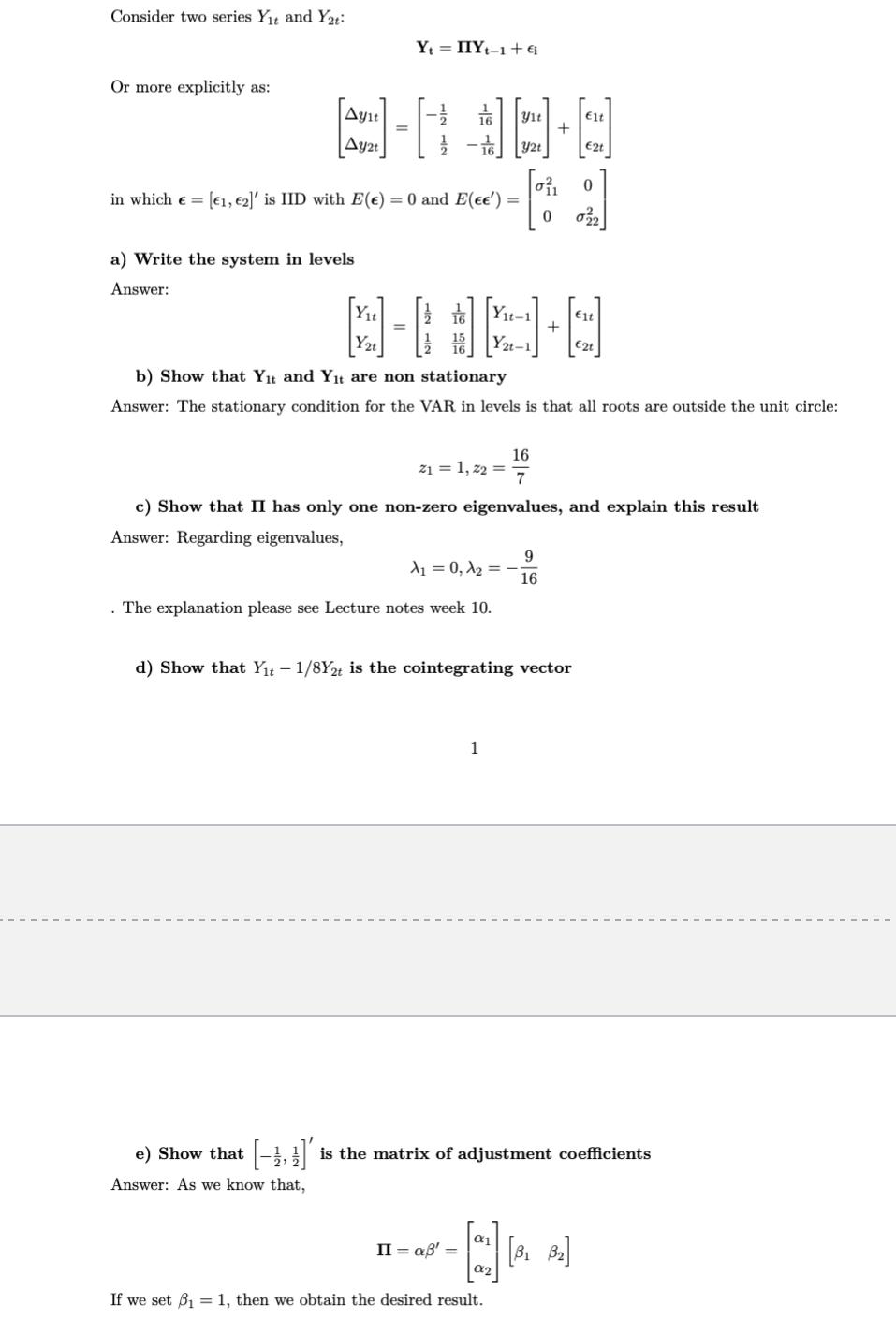

Consider two series Yt and Y2t: Y = IIY-1 +6 Or more explicitly as: Aye Aya Yit Elt + Y2t 2t in which =

Consider two series Yt and Y2t: Y = IIY-1 +6 Or more explicitly as: Aye Aya Yit Elt + Y2t 2t in which = [1, 2]' is IID with E(e) = 0 and E(ee'): [ 0 0 a) Write the system in levels Answer: A-AU-N b) Show that Yt and Yit are non stationary Y2t-1 Answer: The stationary condition for the VAR in levels is that all roots are outside the unit circle: z = 1, z2 = 16 7 c) Show that II has only one non-zero eigenvalues, and explain this result Answer: Regarding eigenvalues, = 0, = 9 16 . The explanation please see Lecture notes week 10. d) Show that Yt - 1/8Y2t is the cointegrating vector 1 e) Show that [,] is the matrix of adjustment coefficients Answer: As we know that, II = a' A- If we set =1, then we obtain the desired result.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

a Writing the system in levels beginbmatrix y1t y2t endbmatrix ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Income Tax Fundamentals 2013

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill

31st Edition

1111972516, 978-1285586618, 1285586611, 978-1285613109, 978-1111972516