Answered step by step

Verified Expert Solution

Question

1 Approved Answer

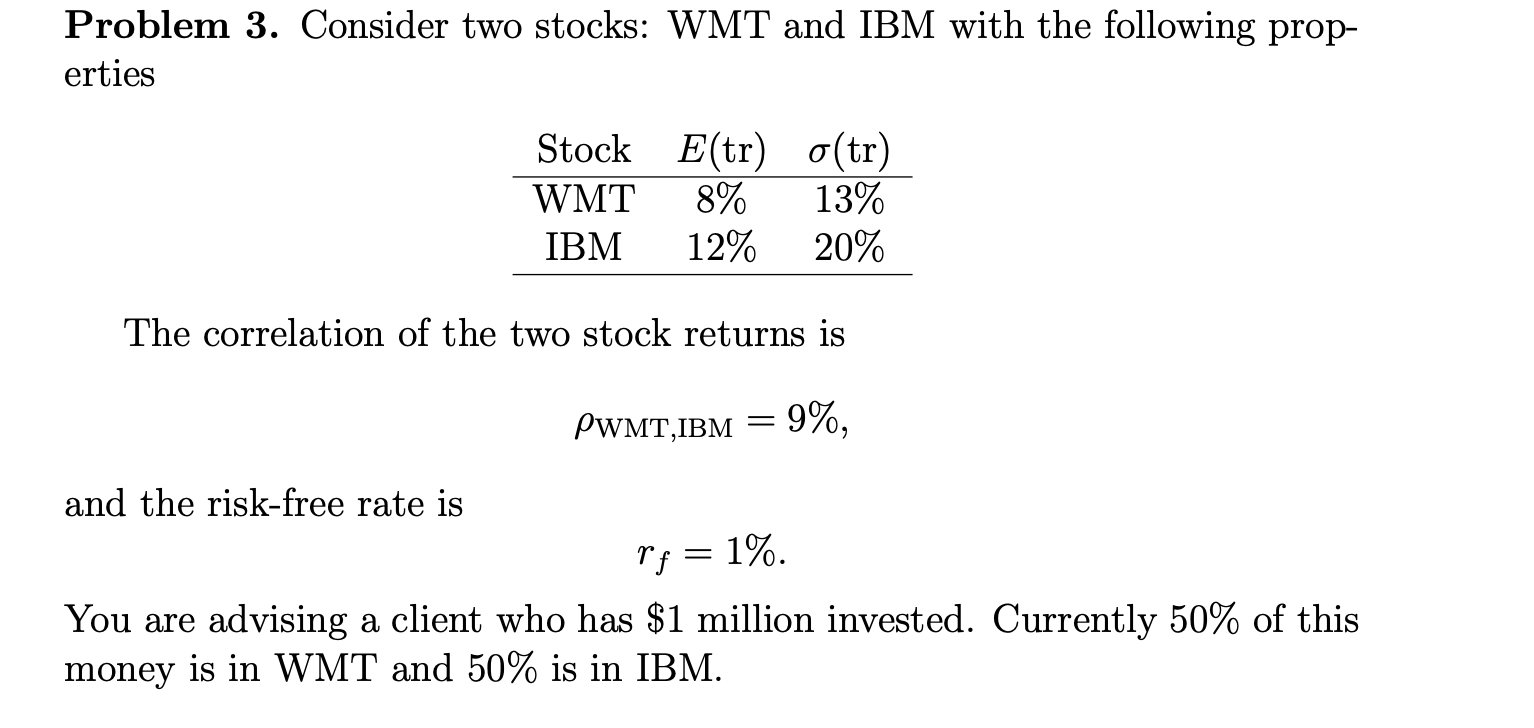

Consider two stocks: WMT and IBM with the following properties: The correlation of the two stock returns is W M T , I B M

Consider two stocks: WMT and IBM with the following properties:

The correlation of the two stock returns is

and the riskfree rate is

You are advising a client who has $ million invested. Currently of this money is in WMT and is in IBM.

You are told that the MVE meanvariance efficient portfolio formed with WMT and IBM has weights wWMT and wIBM

a What are the expected return and standard deviation of the MVE

portfolio?

b What is its Sharpe ratio? How does it compare with the Sharpe

ratio of your clients current portfolio? Explain your finding

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance For Normal People

Authors: Meir Statman

1st Edition

019062647X, 978-0190626471