Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Consider two value processes W and Y that follow a Random Walk with drift, i.e. WW=1H+1HZ1,Z1N(0,1) and YY=2H+2HZ2,Z2N(0,1) and correlation coefficient . Both have an

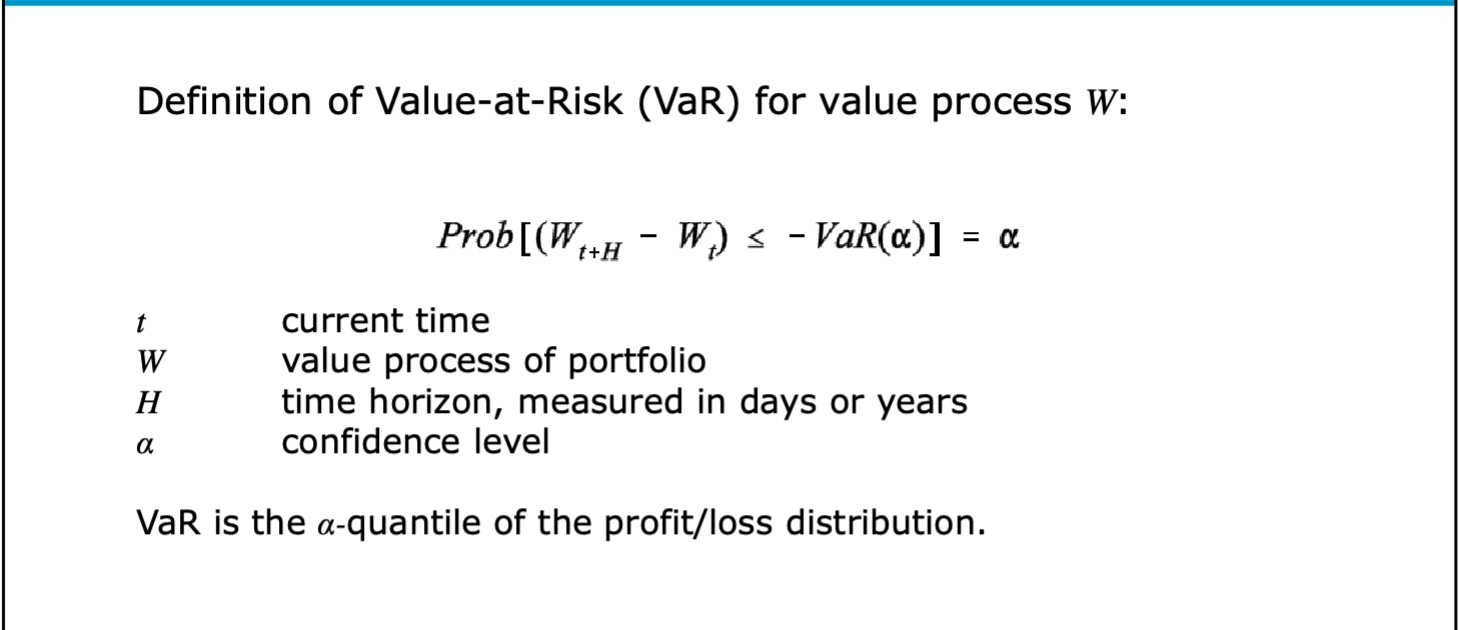

Consider two value processes W and Y that follow a Random Walk with drift, i.e. WW=1H+1HZ1,Z1N(0,1) and YY=2H+2HZ2,Z2N(0,1) and correlation coefficient . Both have an initial value of 80,1=9% p.a., 2=11% p.a., 1=18% p.a., and 2=22% p.a. Assume that you have a portfolio P with an initial value of 80 , and it contains equal weights of both assets W and Y. For which value of is the 1 -year 1% VaR equal to 24.2885 . Hint: Start with writing down the value process of your portfolio and think about its drift and volatility. Additionally, recall that for two assets: =wTw=w1212+w2222+2w1w212 Definition of Value-at-Risk (VaR) for value process W : Prob[(Wt+HWt)VaR()]= t current time W value process of portfolio H time horizon, measured in days or years confidence level

Consider two value processes W and Y that follow a Random Walk with drift, i.e. WW=1H+1HZ1,Z1N(0,1) and YY=2H+2HZ2,Z2N(0,1) and correlation coefficient . Both have an initial value of 80,1=9% p.a., 2=11% p.a., 1=18% p.a., and 2=22% p.a. Assume that you have a portfolio P with an initial value of 80 , and it contains equal weights of both assets W and Y. For which value of is the 1 -year 1% VaR equal to 24.2885 . Hint: Start with writing down the value process of your portfolio and think about its drift and volatility. Additionally, recall that for two assets: =wTw=w1212+w2222+2w1w212 Definition of Value-at-Risk (VaR) for value process W : Prob[(Wt+HWt)VaR()]= t current time W value process of portfolio H time horizon, measured in days or years confidence level Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

School Finance A Policy Perspective

Authors: Allan Odden, Lawrence Picus

5th Edition

0078110289, 978-0078110283