Answered step by step

Verified Expert Solution

Question

1 Approved Answer

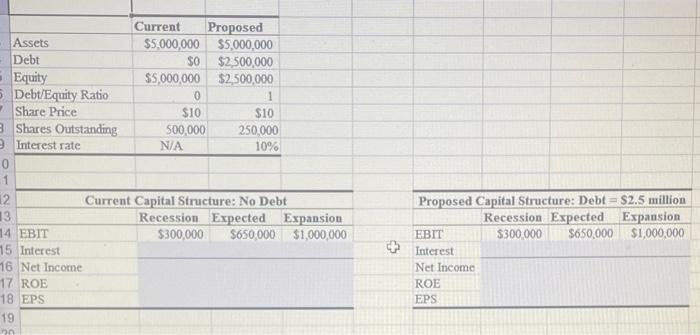

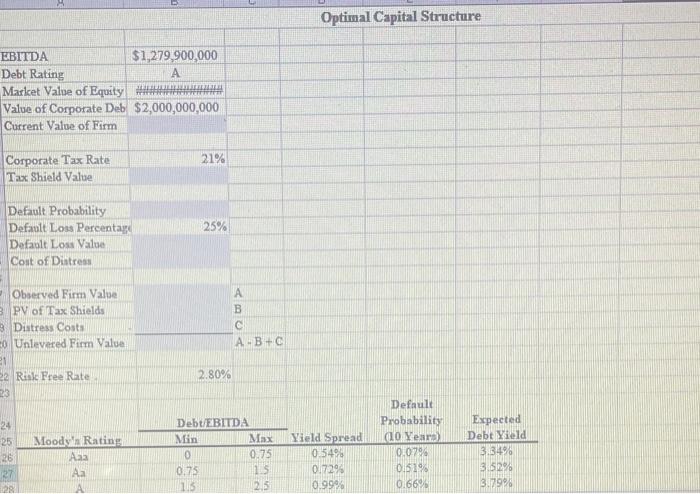

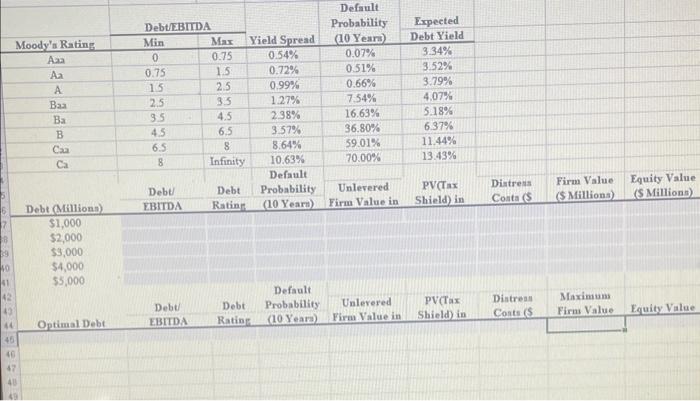

considering replacing half of it with debt. The next example will focus on identifying the optimal capital structure, and the following information may be useful

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Understanding And Auditing IT Systems Volume 1

Authors: Young-Woon Min

2nd Edition

978-1257124084