Answered step by step

Verified Expert Solution

Question

1 Approved Answer

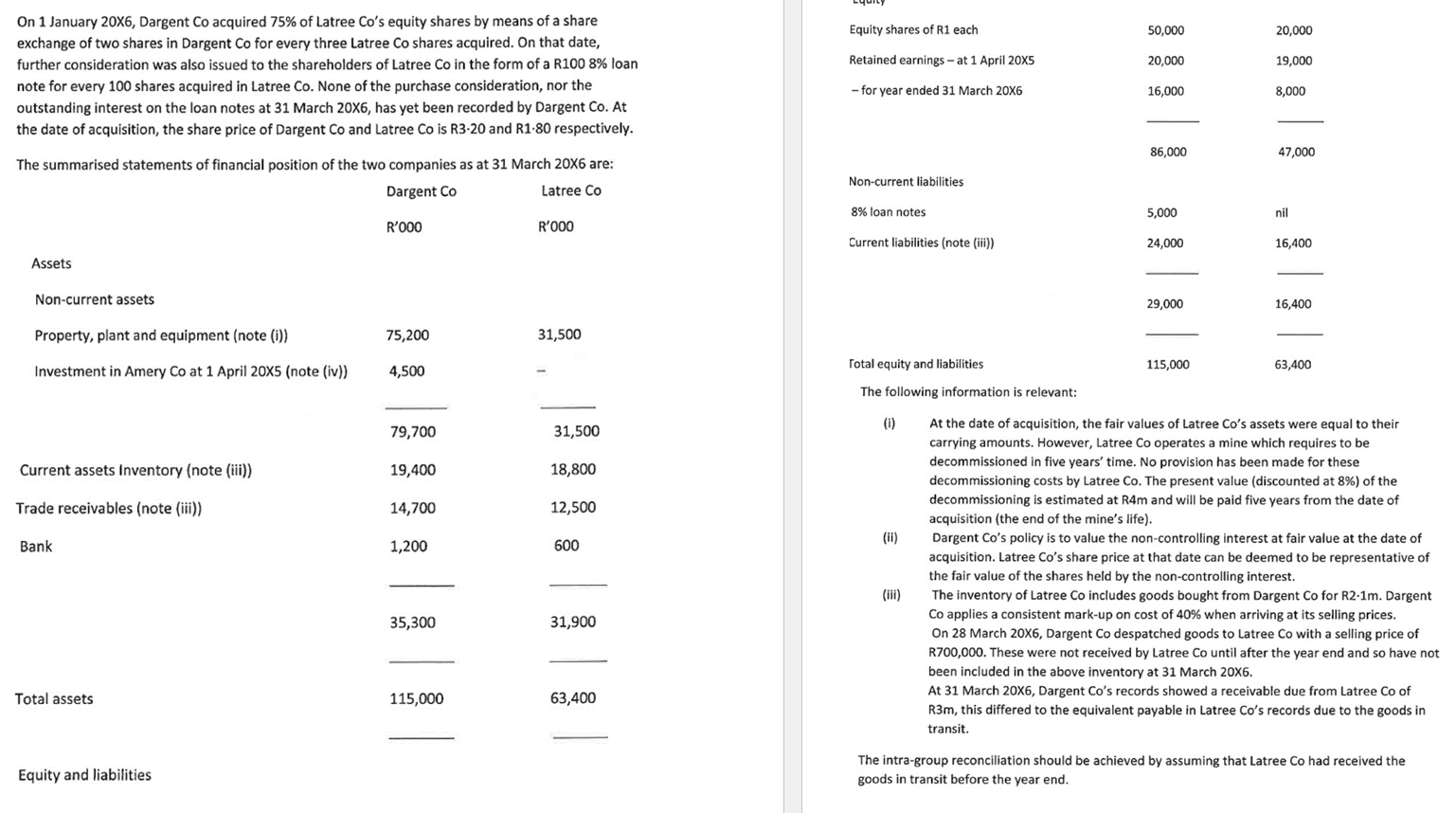

CONSOLIDATED STATEMENT OF FINANCIAL POSITION AND On 1 January 20X6, Dargent Co acquired 75% of Latree Co's equity shares by means of a share exchange

CONSOLIDATED STATEMENT OF FINANCIAL POSITION

AND

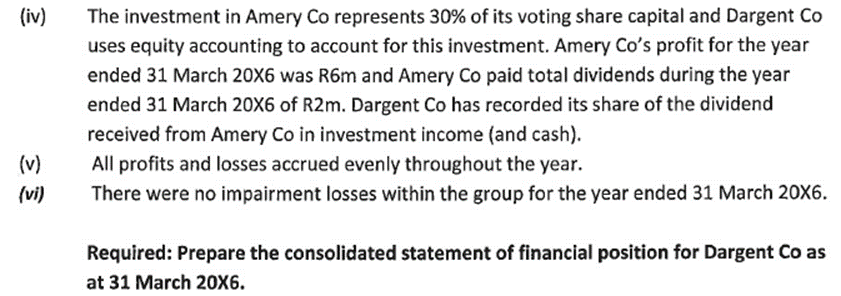

On 1 January 20X6, Dargent Co acquired 75\% of Latree Co's equity shares by means of a share exchange of two shares in Dargent Co for every three Latree Co shares acquired. On that date, further consideration was also issued to the shareholders of Latree Co in the form of a R100 8\% loan note for every 100 shares acquired in Latree Co. None of the purchase consideration, nor the outstanding interest on the loan notes at 31 March 20X6, has yet been recorded by Dargent Co. At the date of acquisition, the share price of Dargent Co0 and Latree CoOiR3.20 and R1.80 respectively. The summarised statements of financial position of the two companies as at 31 March 20X6 are: The following information is relevant: (i) At the date of acquisition, the fair values of Latree Co's assets were equal to their carrying amounts. However, Latree Co operates a mine which requires to be decommissioned in five years' time. No provision has been made for these decommissioning costs by Latree Co. The present value (discounted at 8% ) of the decommissioning is estimated at R4m and will be paid five years from the date of acquisition (the end of the mine's life). (ii) Dargent Co's policy is to value the non-controlling interest at fair value at the date of acquisition. Latree Co's share price at that date can be deemed to be representative of the fair value of the shares held by the non-controlling interest. (iii) The inventory of Latree Co includes goods bought from Dargent Co for R21m. Dargent Co applies a consistent mark-up on cost of 40% when arriving at its selling prices. On 28 March 20X6, Dargent Co despatched goods to Latree Co with a selling price of R700,000. These were not received by Latree Co until after the year end and so have not been included in the above inventory at 31 March 206. At 31 March 20X6, Dargent Co's records showed a receivable due from Latree Co of R3m, this differed to the equivalent payable in Latree Co's records due to the goods in transit. The intra-group reconciliation should be achieved by assuming that Latree Co had received the goods in transit before the year end. (iv) The investment in Amery Co represents 30% of its voting share capital and Dargent Co uses equity accounting to account for this investment. Amery Co's profit for the year ended 31 March 20X6 was R6m and Amery Co paid total dividends during the year ended 31 March 206 of R2m. Dargent Co has recorded its share of the dividend received from Amery Co in investment income (and cash). (v) All profits and losses accrued evenly throughout the year. (vi) There were no impairment losses within the group for the year ended 31 March 20X6. Required: Prepare the consolidated statement of financial position for Dargent Co as at 31 March 206. On 1 January 20X6, Dargent Co acquired 75\% of Latree Co's equity shares by means of a share exchange of two shares in Dargent Co for every three Latree Co shares acquired. On that date, further consideration was also issued to the shareholders of Latree Co in the form of a R100 8\% loan note for every 100 shares acquired in Latree Co. None of the purchase consideration, nor the outstanding interest on the loan notes at 31 March 20X6, has yet been recorded by Dargent Co. At the date of acquisition, the share price of Dargent Co0 and Latree CoOiR3.20 and R1.80 respectively. The summarised statements of financial position of the two companies as at 31 March 20X6 are: The following information is relevant: (i) At the date of acquisition, the fair values of Latree Co's assets were equal to their carrying amounts. However, Latree Co operates a mine which requires to be decommissioned in five years' time. No provision has been made for these decommissioning costs by Latree Co. The present value (discounted at 8% ) of the decommissioning is estimated at R4m and will be paid five years from the date of acquisition (the end of the mine's life). (ii) Dargent Co's policy is to value the non-controlling interest at fair value at the date of acquisition. Latree Co's share price at that date can be deemed to be representative of the fair value of the shares held by the non-controlling interest. (iii) The inventory of Latree Co includes goods bought from Dargent Co for R21m. Dargent Co applies a consistent mark-up on cost of 40% when arriving at its selling prices. On 28 March 20X6, Dargent Co despatched goods to Latree Co with a selling price of R700,000. These were not received by Latree Co until after the year end and so have not been included in the above inventory at 31 March 206. At 31 March 20X6, Dargent Co's records showed a receivable due from Latree Co of R3m, this differed to the equivalent payable in Latree Co's records due to the goods in transit. The intra-group reconciliation should be achieved by assuming that Latree Co had received the goods in transit before the year end. (iv) The investment in Amery Co represents 30% of its voting share capital and Dargent Co uses equity accounting to account for this investment. Amery Co's profit for the year ended 31 March 20X6 was R6m and Amery Co paid total dividends during the year ended 31 March 206 of R2m. Dargent Co has recorded its share of the dividend received from Amery Co in investment income (and cash). (v) All profits and losses accrued evenly throughout the year. (vi) There were no impairment losses within the group for the year ended 31 March 20X6. Required: Prepare the consolidated statement of financial position for Dargent Co as at 31 March 206

On 1 January 20X6, Dargent Co acquired 75\% of Latree Co's equity shares by means of a share exchange of two shares in Dargent Co for every three Latree Co shares acquired. On that date, further consideration was also issued to the shareholders of Latree Co in the form of a R100 8\% loan note for every 100 shares acquired in Latree Co. None of the purchase consideration, nor the outstanding interest on the loan notes at 31 March 20X6, has yet been recorded by Dargent Co. At the date of acquisition, the share price of Dargent Co0 and Latree CoOiR3.20 and R1.80 respectively. The summarised statements of financial position of the two companies as at 31 March 20X6 are: The following information is relevant: (i) At the date of acquisition, the fair values of Latree Co's assets were equal to their carrying amounts. However, Latree Co operates a mine which requires to be decommissioned in five years' time. No provision has been made for these decommissioning costs by Latree Co. The present value (discounted at 8% ) of the decommissioning is estimated at R4m and will be paid five years from the date of acquisition (the end of the mine's life). (ii) Dargent Co's policy is to value the non-controlling interest at fair value at the date of acquisition. Latree Co's share price at that date can be deemed to be representative of the fair value of the shares held by the non-controlling interest. (iii) The inventory of Latree Co includes goods bought from Dargent Co for R21m. Dargent Co applies a consistent mark-up on cost of 40% when arriving at its selling prices. On 28 March 20X6, Dargent Co despatched goods to Latree Co with a selling price of R700,000. These were not received by Latree Co until after the year end and so have not been included in the above inventory at 31 March 206. At 31 March 20X6, Dargent Co's records showed a receivable due from Latree Co of R3m, this differed to the equivalent payable in Latree Co's records due to the goods in transit. The intra-group reconciliation should be achieved by assuming that Latree Co had received the goods in transit before the year end. (iv) The investment in Amery Co represents 30% of its voting share capital and Dargent Co uses equity accounting to account for this investment. Amery Co's profit for the year ended 31 March 20X6 was R6m and Amery Co paid total dividends during the year ended 31 March 206 of R2m. Dargent Co has recorded its share of the dividend received from Amery Co in investment income (and cash). (v) All profits and losses accrued evenly throughout the year. (vi) There were no impairment losses within the group for the year ended 31 March 20X6. Required: Prepare the consolidated statement of financial position for Dargent Co as at 31 March 206. On 1 January 20X6, Dargent Co acquired 75\% of Latree Co's equity shares by means of a share exchange of two shares in Dargent Co for every three Latree Co shares acquired. On that date, further consideration was also issued to the shareholders of Latree Co in the form of a R100 8\% loan note for every 100 shares acquired in Latree Co. None of the purchase consideration, nor the outstanding interest on the loan notes at 31 March 20X6, has yet been recorded by Dargent Co. At the date of acquisition, the share price of Dargent Co0 and Latree CoOiR3.20 and R1.80 respectively. The summarised statements of financial position of the two companies as at 31 March 20X6 are: The following information is relevant: (i) At the date of acquisition, the fair values of Latree Co's assets were equal to their carrying amounts. However, Latree Co operates a mine which requires to be decommissioned in five years' time. No provision has been made for these decommissioning costs by Latree Co. The present value (discounted at 8% ) of the decommissioning is estimated at R4m and will be paid five years from the date of acquisition (the end of the mine's life). (ii) Dargent Co's policy is to value the non-controlling interest at fair value at the date of acquisition. Latree Co's share price at that date can be deemed to be representative of the fair value of the shares held by the non-controlling interest. (iii) The inventory of Latree Co includes goods bought from Dargent Co for R21m. Dargent Co applies a consistent mark-up on cost of 40% when arriving at its selling prices. On 28 March 20X6, Dargent Co despatched goods to Latree Co with a selling price of R700,000. These were not received by Latree Co until after the year end and so have not been included in the above inventory at 31 March 206. At 31 March 20X6, Dargent Co's records showed a receivable due from Latree Co of R3m, this differed to the equivalent payable in Latree Co's records due to the goods in transit. The intra-group reconciliation should be achieved by assuming that Latree Co had received the goods in transit before the year end. (iv) The investment in Amery Co represents 30% of its voting share capital and Dargent Co uses equity accounting to account for this investment. Amery Co's profit for the year ended 31 March 20X6 was R6m and Amery Co paid total dividends during the year ended 31 March 206 of R2m. Dargent Co has recorded its share of the dividend received from Amery Co in investment income (and cash). (v) All profits and losses accrued evenly throughout the year. (vi) There were no impairment losses within the group for the year ended 31 March 20X6. Required: Prepare the consolidated statement of financial position for Dargent Co as at 31 March 206 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Exam Prep For Financial And Managerial Accounting The Basis For Business Decisions By Williams Et Al 13th Ed

Authors: Mznlnx

13th Edition

1428871764, 978-1428871762