Answered step by step

Verified Expert Solution

Question

1 Approved Answer

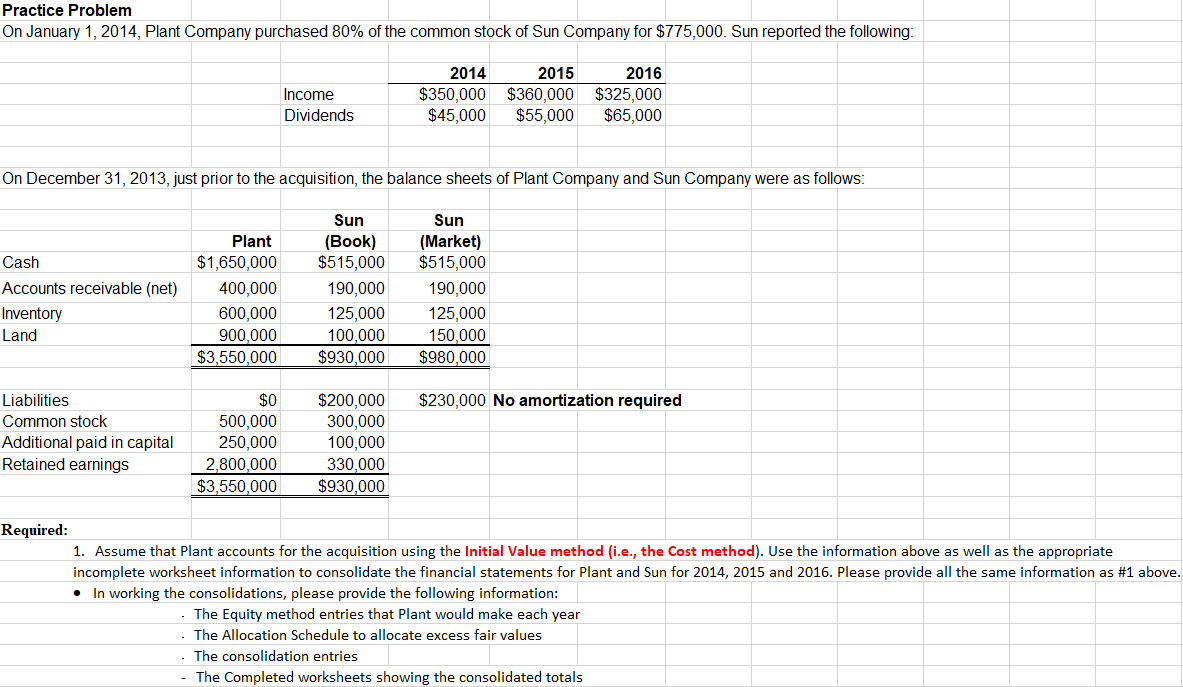

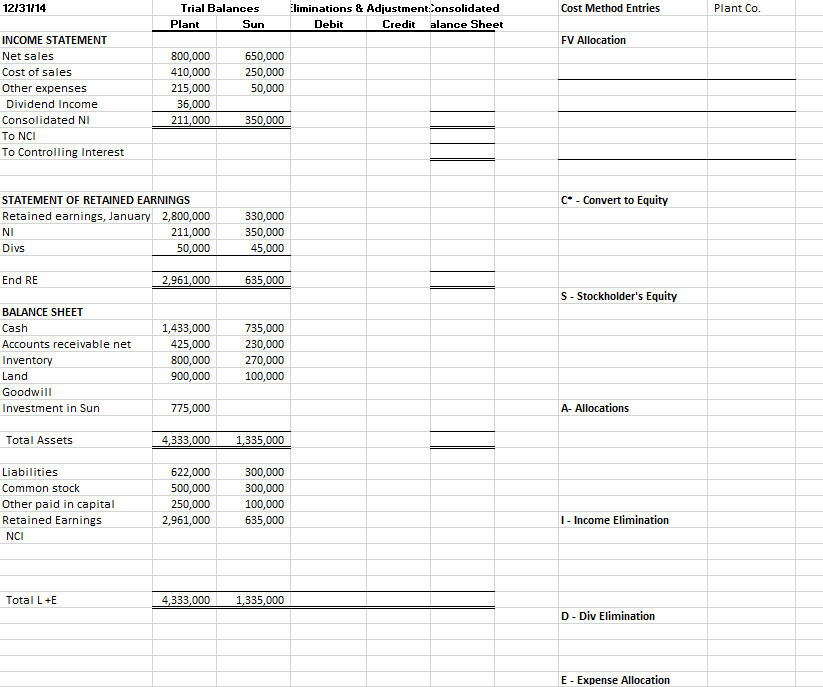

Consolidation case cost method Practice Problem On January 1, 2014, Plant Company purchased 80% of the common stock of Sun Company for $775,000. Sun reported

Consolidation case cost method

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Electronic Working Papers For Needles Powers Crossons Financial And Managerial Accounting 9th And Crosson Needles Managerial Accounting

Authors: Susan V. Crosson, Belverd E. Needles

9th Edition

0538791918, 978-0538791915