Consolidation Problem (20 questions, 5 marks each, 100 marks in total)

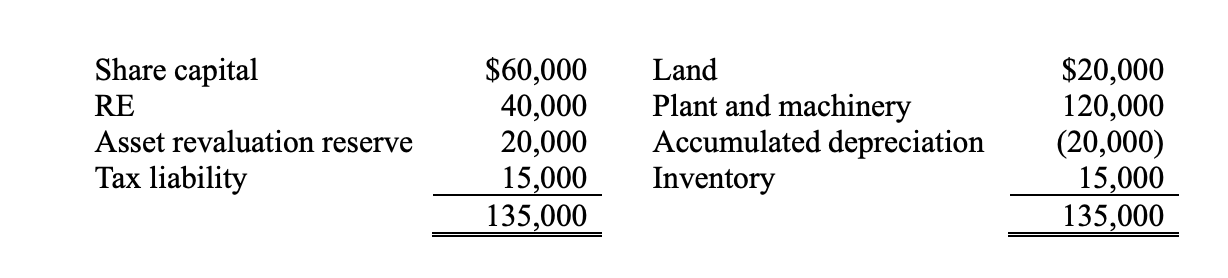

P Ltd gained control of S Ltd by acquiring all its share capital on 1 Jan 2010. The FV of the consideration paid was measured at $114,000. The statement of financial position of S Ltd at that date showed:

At 1 Jan 2010, the recorded amounts of S Ltds assets and liabilities were equal to their fair values except as follows:

Of the inventory on hand at 1 Jan 2010, 30% was sold by 31 Dec 2010, 30% was sold by 31 Dec 2011, and the remaining 40% was sold by 31 Dec 2012. The plant and machinery have a further 5-year life and are depreciated on a straight-line basis. At 1 Jan 2010, S Ltd was involved in a court case with an entity that was claiming damages from it. S Ltd had not recognized any liability in relation to the possible damages. P Ltd measured the fair value of the liability at $5,000. In March 2012, S Ltd lost the court case and a payment of $7,000 was made on 1 April 2012. Tax rate is 30%.

On June 2011, P Ltd sold inventory to S Ltd for $15,000. This inventory had previously cost P Ltd $8,000, and 80% of this inventory remained unsold by S Ltd at the end of 2011. At the end of 2012, half of this remaining inventory was still on hand. On 1 July 2010, S Ltd sold an item of plant to P Ltd for $100,000. The carrying amount of this plant on S Ltd accounts is $80,000. S Ltd used the straight-line method over 10 years and P Ltd depreciated this plant at 10% p.a. on the diminishing value.

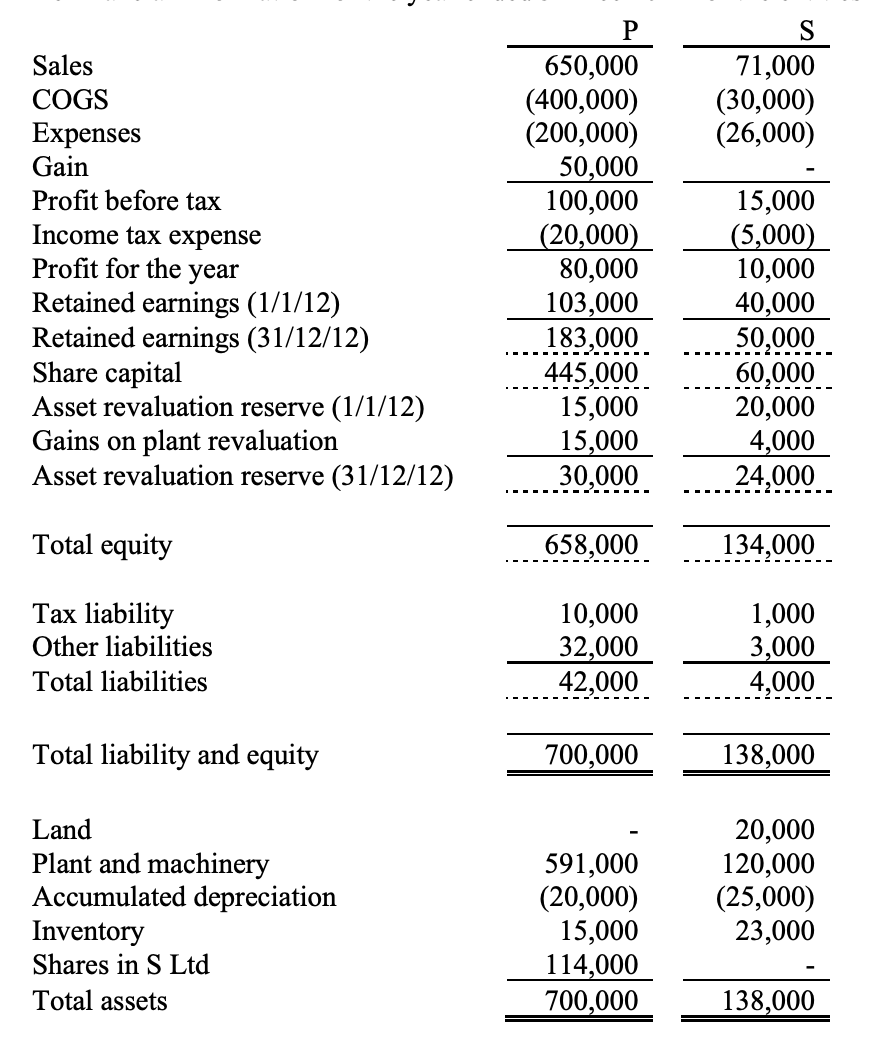

The financial information for the year ended 31 Dec 2012 for the entities within the group was as follows: PS

Note: Expenses includes depreciation expense, settlement of lawsuits and all the other expenses other than COGS.

Required:

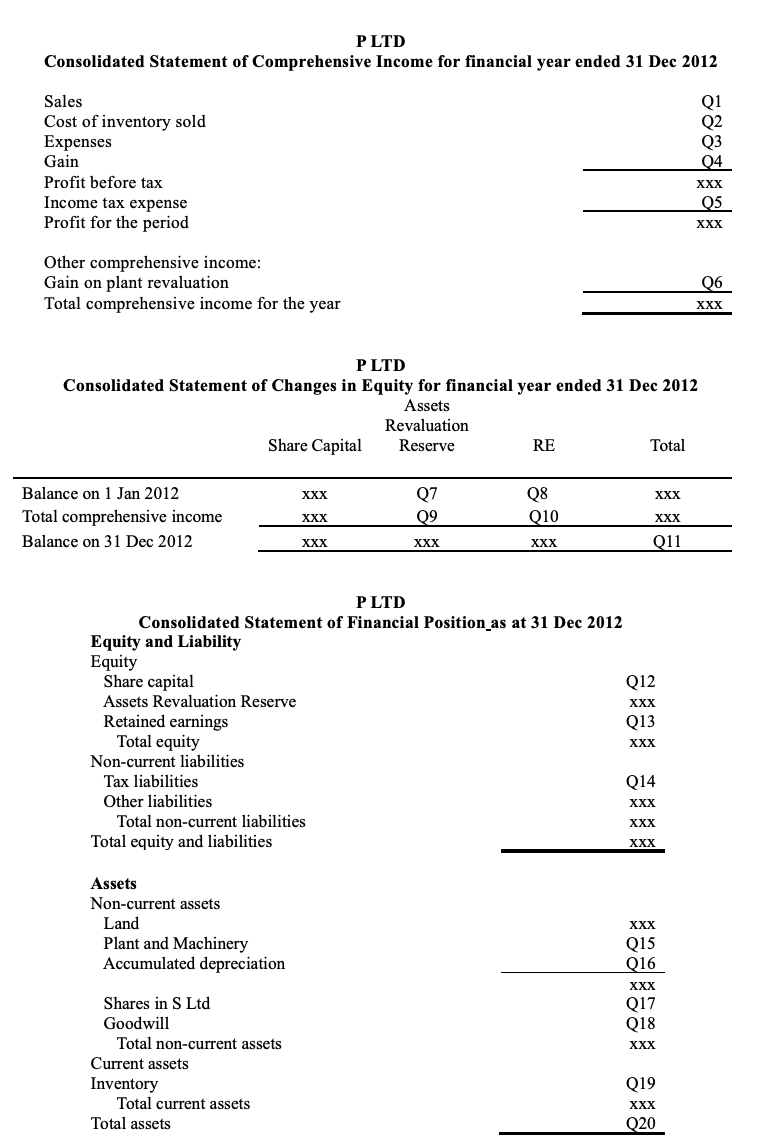

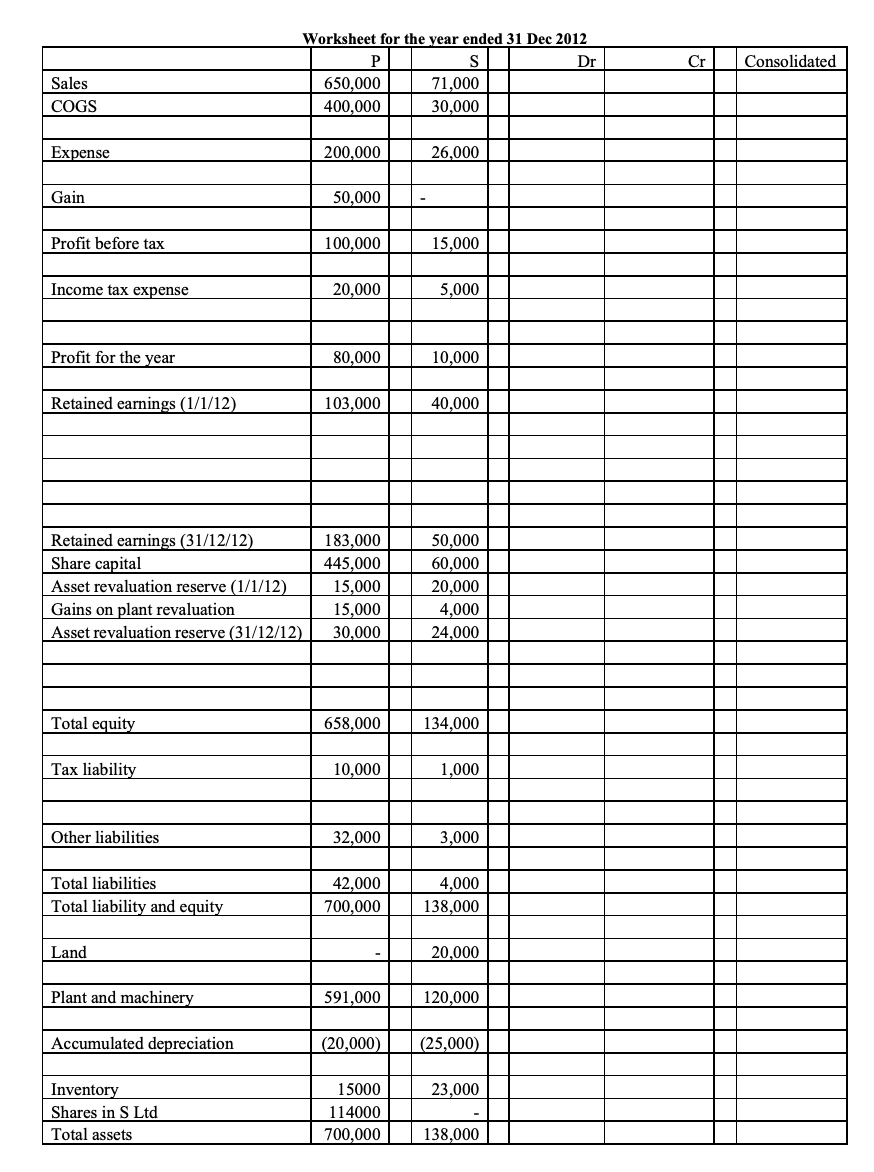

Determine the amounts that are to be reported in the consolidated financial statements of P Ltd for the year ended 31 Dec 2012, as indicated by Q1 to Q20.

Share capital RE Asset revaluation reserve Tax liability $60,000 40,000 20,000 15,000 135,000 Land Plant and machinery Accumulated depreciation Inventory $20,000 120,000 (20,000) 15,000 135,000 Inventory Plant and machinery Carrying amount $15,000 100,000 FV $18,000 102,000 S 71,000 (30,000) (26,000) Sales COGS Expenses Gain Profit before tax Income tax expense Profit for the year Retained earnings (1/1/12) Retained earnings (31/12/12) Share capital Asset revaluation reserve (1/1/12) Gains on plant revaluation Asset revaluation reserve (31/12/12) P 650,000 (400,000) (200,000) 50,000 100,000 (20,000) 80,000 103,000 183,000 445,000 15,000 15,000 30,000 15,000 (5,000) 10,000 40,000 50,000 60,000 20,000 4,000 24,000 Total equity 658,000 134,000 Tax liability Other liabilities Total liabilities 10,000 32,000 42,000 1,000 3,000 4,000 Total liability and equity 700,000 138,000 Land Plant and machinery Accumulated depreciation Inventory Shares in S Ltd Total assets 591,000 (20,000) 15,000 114,000 700,000 20,000 120,000 (25,000) 23,000 138,000 P LTD Consolidated Statement of Comprehensive Income for financial year ended 31 Dec 2012 Sales Cost of inventory sold Expenses Gain Profit before tax Income tax expense Profit for the period Q1 Q2 Q3 04 XXX Q5 XXX Other comprehensive income: Gain on plant revaluation Total comprehensive income for the year 06 XXX P LTD Consolidated Statement of Changes in Equity for financial year ended 31 Dec 2012 Assets Revaluation Share Capital Reserve RE Total XXX XXX Balance on 1 Jan 2012 Total comprehensive income Balance on 31 Dec 2012 Q7 09 Q8 Q10 XXX XXX XXX XXX XXX Q11 P LTD Consolidated Statement of Financial Position as at 31 Dec 2012 Equity and Liability Equity Share capital Q12 Assets Revaluation Reserve XXX Retained earnings 013 Total equity XXX Non-current liabilities Tax liabilities Q14 Other liabilities XXX Total non-current liabilities XXX Total equity and liabilities XXX Assets Non-current assets Land Plant and Machinery Accumulated depreciation XXX Q15 Q16 XXX Q17 Q18 XXX Shares in S Ltd Goodwill Total non-current assets Current assets Inventory Total current assets Total assets 019 XXX Q20 Cr Consolidated Worksheet for the year ended 31 Dec 2012 S Dr 650,000 71,000 400,000 30,000 Sales COGS Expense 200,000 26,000 Gain 50,000 Profit before tax 100,000 15,000 Income tax expense 20,000 5,000 Profit for the year 80,000 10,000 Retained earnings (1/1/12) 103,000 40,000 Retained earnings (31/12/12) Share capital Asset revaluation reserve (1/1/12) Gains on plant revaluation Asset revaluation reserve (31/12/12) 183,000 445,000 15,000 15,000 30,000 50,000 60,000 20,000 4,000 24,000 Total equity 658,000 134,000 Tax liability 10,000 1,000 Other liabilities 32,000 3,000 Total liabilities Total liability and equity 42,000 700,000 4,000 138,000 Land 20,000 Plant and machinery 591,000 120,000 Accumulated depreciation (20,000) (25,000 23,000 Inventory Shares in S Ltd Total assets 15000 114000 700,000 138,000 Share capital RE Asset revaluation reserve Tax liability $60,000 40,000 20,000 15,000 135,000 Land Plant and machinery Accumulated depreciation Inventory $20,000 120,000 (20,000) 15,000 135,000 Inventory Plant and machinery Carrying amount $15,000 100,000 FV $18,000 102,000 S 71,000 (30,000) (26,000) Sales COGS Expenses Gain Profit before tax Income tax expense Profit for the year Retained earnings (1/1/12) Retained earnings (31/12/12) Share capital Asset revaluation reserve (1/1/12) Gains on plant revaluation Asset revaluation reserve (31/12/12) P 650,000 (400,000) (200,000) 50,000 100,000 (20,000) 80,000 103,000 183,000 445,000 15,000 15,000 30,000 15,000 (5,000) 10,000 40,000 50,000 60,000 20,000 4,000 24,000 Total equity 658,000 134,000 Tax liability Other liabilities Total liabilities 10,000 32,000 42,000 1,000 3,000 4,000 Total liability and equity 700,000 138,000 Land Plant and machinery Accumulated depreciation Inventory Shares in S Ltd Total assets 591,000 (20,000) 15,000 114,000 700,000 20,000 120,000 (25,000) 23,000 138,000 P LTD Consolidated Statement of Comprehensive Income for financial year ended 31 Dec 2012 Sales Cost of inventory sold Expenses Gain Profit before tax Income tax expense Profit for the period Q1 Q2 Q3 04 XXX Q5 XXX Other comprehensive income: Gain on plant revaluation Total comprehensive income for the year 06 XXX P LTD Consolidated Statement of Changes in Equity for financial year ended 31 Dec 2012 Assets Revaluation Share Capital Reserve RE Total XXX XXX Balance on 1 Jan 2012 Total comprehensive income Balance on 31 Dec 2012 Q7 09 Q8 Q10 XXX XXX XXX XXX XXX Q11 P LTD Consolidated Statement of Financial Position as at 31 Dec 2012 Equity and Liability Equity Share capital Q12 Assets Revaluation Reserve XXX Retained earnings 013 Total equity XXX Non-current liabilities Tax liabilities Q14 Other liabilities XXX Total non-current liabilities XXX Total equity and liabilities XXX Assets Non-current assets Land Plant and Machinery Accumulated depreciation XXX Q15 Q16 XXX Q17 Q18 XXX Shares in S Ltd Goodwill Total non-current assets Current assets Inventory Total current assets Total assets 019 XXX Q20 Cr Consolidated Worksheet for the year ended 31 Dec 2012 S Dr 650,000 71,000 400,000 30,000 Sales COGS Expense 200,000 26,000 Gain 50,000 Profit before tax 100,000 15,000 Income tax expense 20,000 5,000 Profit for the year 80,000 10,000 Retained earnings (1/1/12) 103,000 40,000 Retained earnings (31/12/12) Share capital Asset revaluation reserve (1/1/12) Gains on plant revaluation Asset revaluation reserve (31/12/12) 183,000 445,000 15,000 15,000 30,000 50,000 60,000 20,000 4,000 24,000 Total equity 658,000 134,000 Tax liability 10,000 1,000 Other liabilities 32,000 3,000 Total liabilities Total liability and equity 42,000 700,000 4,000 138,000 Land 20,000 Plant and machinery 591,000 120,000 Accumulated depreciation (20,000) (25,000 23,000 Inventory Shares in S Ltd Total assets 15000 114000 700,000 138,000