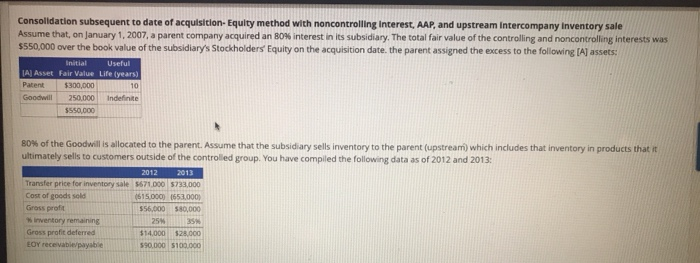

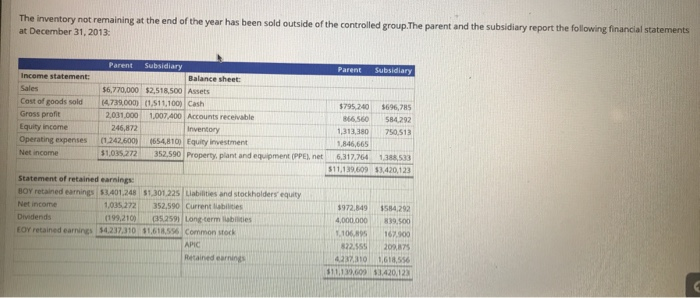

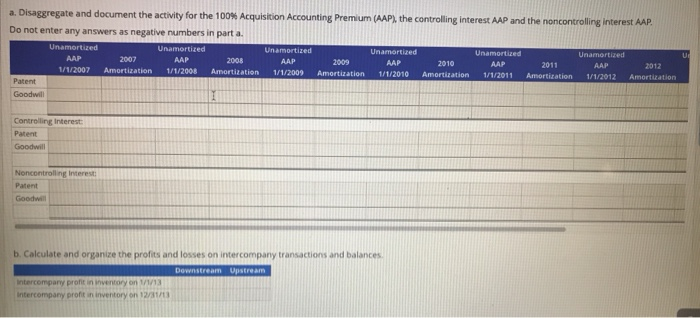

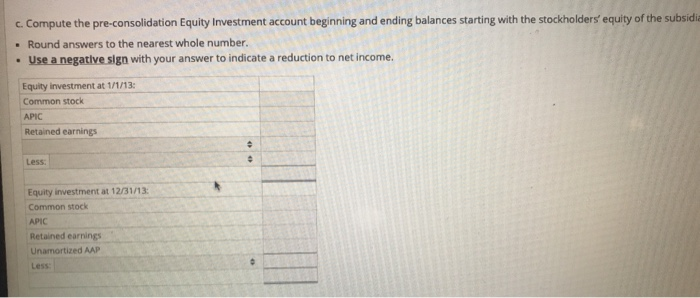

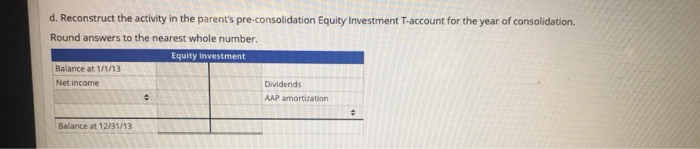

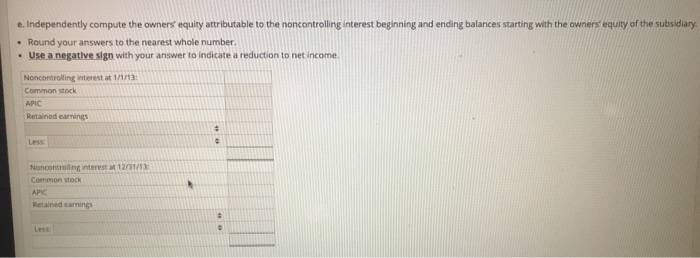

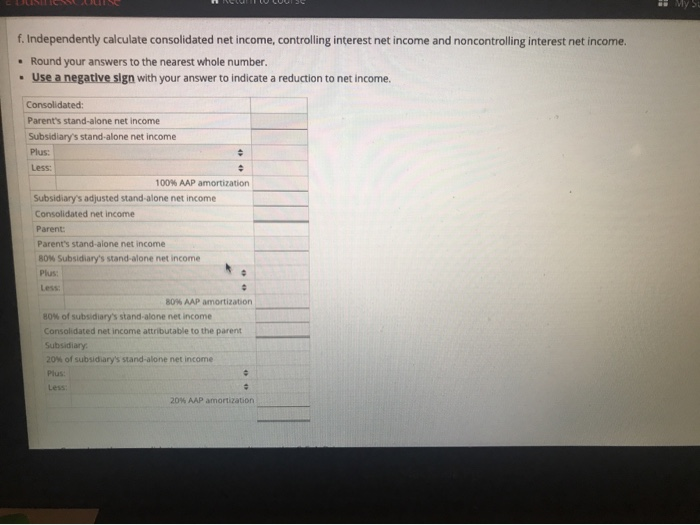

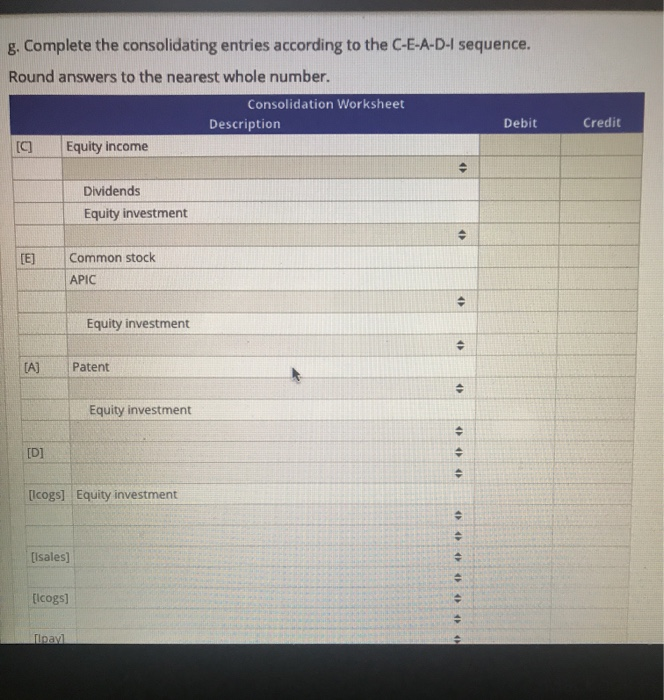

Consolidation subsequent to date of acquisition- Equity method with noncontrolling Interest, AAP, and upstream Intercompany inventory sale Assume that, on January 1, 2007, a parent company acquired an 80% interest in its subsidiary. The total fair value of the controlling and noncontrolling interests was $550,000 over the book value of the subsidiary's Stockholders Equity on the acquisition date, the parent assigned the excess to the following [A] assets: Initial Useful LAI Asset Fair Value Life (years) P 500.000 Goodwill 250.000 indefinite 550.000 80% of the Goodwill is allocated to the parent. Assume that the subsidiary sells inventory to the parent (upstream) which includes that inventory in products that it ultimately sells to customers outside of the controlled group. You have compiled the following data as of 2012 and 2013: 2012 2013 Transfer price for inventory Sale $571 DOO 5733.000 Cost of goods sold 515.000 1652000 380,000 inventory remaining Gross profit deferred EGY recevable payable 590.000 $10000 The inventory not remaining at the end of the year has been sold outside of the controlled group. The parent and the subsidiary report the following financial statements at December 31, 2013: Parent Subsidiary income statement Cost of goods sold $795.240 Parent Subsidiary Balance sheet $6,770,000 $2,518,500 Assets 14.739.000) (1.511,100 Cash 2001 000 1007 400 Accounts receivable 245,872 Inventory (1.242.600) 1654,810) Equity investment $1.035 272 352.590 Property, plant and woment (PPEnet Gross of 5696,785 5840292 20513 3133 Equity income Operating expenses Net income 6,217,764 $11.139.609 18533 420,123 Statement of retained earning BOY retained ning 1.401.248 51 301.225 Limbs and stockholders' equity Net income 1,035 272 352,590 Current abilities Dividends 1199, 2101 35259) Long term bilities for retained earnings 237.310 Solasso common stock $972.149 4,000,000 106 22 110 154292 39.500 167.500 2007 16.556 1420 121 Retained earnings $11,13,600 a. Disaggregate and document the activity for the 100% Acquisition Accounting Premium (AAP), the controlling interest AAP and the noncontrolling interest AAP. Do not enter any answers as negative numbers in part a. Unamortized Unamortized Unamortized Unamortized Unamortized Unamortized AAP 2007 AAP 2008 AAP 2009 AAP 2010 AAP 2011 AAP 2012 1/11/2007 Amortization 1/1/2008 Amortization 11/2009 Amortization 1/1/2010 Amortization 11/2011 Amortization 1/1/2012 Amortization Patent Goodwill Controlling interest Goodwill Noncontrolling interes Patent b. Calculate and organize the profits and losses on intercompany transactions and balances Destream stream Intercompany profi o n 3 Intercompany profit in invertory on c. Compute the pre-consolidation Equity Investment account beginning and ending balances starting with the stockholders' equity of the subsidi . Round answers to the nearest whole number. Use a negative sign with your answer to indicate a reduction to net income. Equity investment at 1/1/13 Common stock APIC Retained earnings Less Equity investment at 12/31/13 Common stock Retained earnings Unamortized MAP d. Reconstruct the activity in the parent's pre-consolidation Equity Investment T-account for the year of consolidation Round answers to the nearest whole number Equity Investment Balance at 1/1/13 Net income Dividends AAP amortization Balance at 12/31/13 e. Independently compute the owners' equity attributable to the noncontrolling interest beginning and ending balances starting with the owners' equity of the subsidiary Round your answers to the nearest whole number. Use a negative sign with your answer to indicate a reduction to net income Noncontrolling interest at 1/1/13 Common stock APIC Retained earnings Less: Noncontrolling interest M12/31/13: Common stock APIC Retained earnings f. Independently calculate consolidated net income, controlling interest net income and noncontrolling interest net income. Round your answers to the nearest whole number. Use a negative sign with your answer to indicate a reduction to net income. Consolidated: Parent's stand-alone net income Subsidiary's stand-alone net income Plus 100% AAP amortization Subsidiary's adjusted stand-alone net income Consolidated net income Parent Parent's stand-alone net income BOX Subsidiary's stand-alone net income Plus Less BO AAP amortization 80% of subsidiary's stand-alone net income Consolidated net income attributable to the parent Subsidiary 20% of subsidiary's stand-alone net income Plus: 20 AAP amortization g. Complete the consolidating entries according to the C-E-A-D-I sequence. Round answers to the nearest whole number. Consolidation Worksheet Description Equity income Debit Credit [C] Dividends Equity investment Common stock APIC Equity investment (A) Patent Equity investment [D] [lcogs] Equity investment [lsales] [lcogs] Tupayl Equity investment [E] Common stock APIC Equity investment [A] Patent Equity investment [D] [lcogs] Equity investment [Isales] [lcogs] [lpayl Consolidation subsequent to date of acquisition- Equity method with noncontrolling Interest, AAP, and upstream Intercompany inventory sale Assume that, on January 1, 2007, a parent company acquired an 80% interest in its subsidiary. The total fair value of the controlling and noncontrolling interests was $550,000 over the book value of the subsidiary's Stockholders Equity on the acquisition date, the parent assigned the excess to the following [A] assets: Initial Useful LAI Asset Fair Value Life (years) P 500.000 Goodwill 250.000 indefinite 550.000 80% of the Goodwill is allocated to the parent. Assume that the subsidiary sells inventory to the parent (upstream) which includes that inventory in products that it ultimately sells to customers outside of the controlled group. You have compiled the following data as of 2012 and 2013: 2012 2013 Transfer price for inventory Sale $571 DOO 5733.000 Cost of goods sold 515.000 1652000 380,000 inventory remaining Gross profit deferred EGY recevable payable 590.000 $10000 The inventory not remaining at the end of the year has been sold outside of the controlled group. The parent and the subsidiary report the following financial statements at December 31, 2013: Parent Subsidiary income statement Cost of goods sold $795.240 Parent Subsidiary Balance sheet $6,770,000 $2,518,500 Assets 14.739.000) (1.511,100 Cash 2001 000 1007 400 Accounts receivable 245,872 Inventory (1.242.600) 1654,810) Equity investment $1.035 272 352.590 Property, plant and woment (PPEnet Gross of 5696,785 5840292 20513 3133 Equity income Operating expenses Net income 6,217,764 $11.139.609 18533 420,123 Statement of retained earning BOY retained ning 1.401.248 51 301.225 Limbs and stockholders' equity Net income 1,035 272 352,590 Current abilities Dividends 1199, 2101 35259) Long term bilities for retained earnings 237.310 Solasso common stock $972.149 4,000,000 106 22 110 154292 39.500 167.500 2007 16.556 1420 121 Retained earnings $11,13,600 a. Disaggregate and document the activity for the 100% Acquisition Accounting Premium (AAP), the controlling interest AAP and the noncontrolling interest AAP. Do not enter any answers as negative numbers in part a. Unamortized Unamortized Unamortized Unamortized Unamortized Unamortized AAP 2007 AAP 2008 AAP 2009 AAP 2010 AAP 2011 AAP 2012 1/11/2007 Amortization 1/1/2008 Amortization 11/2009 Amortization 1/1/2010 Amortization 11/2011 Amortization 1/1/2012 Amortization Patent Goodwill Controlling interest Goodwill Noncontrolling interes Patent b. Calculate and organize the profits and losses on intercompany transactions and balances Destream stream Intercompany profi o n 3 Intercompany profit in invertory on c. Compute the pre-consolidation Equity Investment account beginning and ending balances starting with the stockholders' equity of the subsidi . Round answers to the nearest whole number. Use a negative sign with your answer to indicate a reduction to net income. Equity investment at 1/1/13 Common stock APIC Retained earnings Less Equity investment at 12/31/13 Common stock Retained earnings Unamortized MAP d. Reconstruct the activity in the parent's pre-consolidation Equity Investment T-account for the year of consolidation Round answers to the nearest whole number Equity Investment Balance at 1/1/13 Net income Dividends AAP amortization Balance at 12/31/13 e. Independently compute the owners' equity attributable to the noncontrolling interest beginning and ending balances starting with the owners' equity of the subsidiary Round your answers to the nearest whole number. Use a negative sign with your answer to indicate a reduction to net income Noncontrolling interest at 1/1/13 Common stock APIC Retained earnings Less: Noncontrolling interest M12/31/13: Common stock APIC Retained earnings f. Independently calculate consolidated net income, controlling interest net income and noncontrolling interest net income. Round your answers to the nearest whole number. Use a negative sign with your answer to indicate a reduction to net income. Consolidated: Parent's stand-alone net income Subsidiary's stand-alone net income Plus 100% AAP amortization Subsidiary's adjusted stand-alone net income Consolidated net income Parent Parent's stand-alone net income BOX Subsidiary's stand-alone net income Plus Less BO AAP amortization 80% of subsidiary's stand-alone net income Consolidated net income attributable to the parent Subsidiary 20% of subsidiary's stand-alone net income Plus: 20 AAP amortization g. Complete the consolidating entries according to the C-E-A-D-I sequence. Round answers to the nearest whole number. Consolidation Worksheet Description Equity income Debit Credit [C] Dividends Equity investment Common stock APIC Equity investment (A) Patent Equity investment [D] [lcogs] Equity investment [lsales] [lcogs] Tupayl Equity investment [E] Common stock APIC Equity investment [A] Patent Equity investment [D] [lcogs] Equity investment [Isales] [lcogs] [lpayl