Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Construct the Global Minimum-Variance Portfolio (GMVP) consisting of the 5 selected stocks over the April 2017 March 2021 period. Note: You need to do the

Construct the Global Minimum-Variance Portfolio (GMVP) consisting of the 5 selected stocks over the April 2017 March 2021 period.

Note: You need to do the calculation based on the MPT.

- What are the weights of the selected 5 stocks in the GMVP?

- What is the monthly expected return on the GMVP?

- What is the risk of the GMVP (as measured by standard deviation and variance, respectively)?

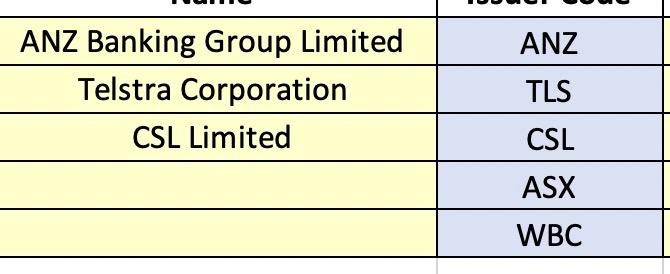

ANZ ANZ Banking Group Limited Telstra Corporation CSL Limited TLS CSL ASX WBC ANZ ANZ Banking Group Limited Telstra Corporation CSL Limited TLS CSL ASX WBC

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Avoiding Bear Traps Easy Macro Factors For Smart Traders

Authors: Kara Boniecka

1st Edition

1502472090, 978-1502472090